Individual

Individual

Participating policy - Annual Benefit Statement - Key Parameters

Key details related to the Annual Benefit Statement for policyholders of participating policies issued by Axis Max Life Insurance Limited, henceforth referred to as “Company”

The Asset Share for a group of policies at a given point in time is the accumulation of the premiums received plus investment income earned from the inception of those policies, less deductions like claim payments, commission, expenses, tax, cost of capital/guarantee charges, contribution from miscellaneous profits/losses (e.g. profits from surrenders/lapses) and any transfers to shareholders.

- The Premiums received component represents the amount of premium paid by the policyholder till the date of computation of asset share.

- Investment income represents the income earned from assets, where the policyholders’ money is getting invested. Axis Max Life Insurance company invests in line with the Regulations issued by the IRDAI with the goal of earning superior risk adjusted returns.

The investments under participating business are generated by investing premiums across two primary asset classes:

• Fixed Interest Securities (like Government bonds and corporate bonds), and

• Growth assets (like stocks, real estate etc).

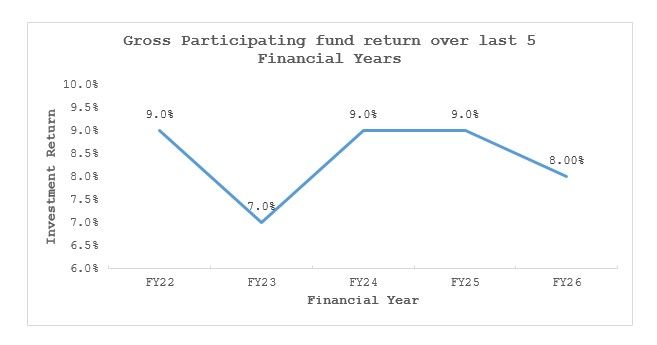

For the financial year 2025-26, the Participating fund achieved an overall return of 8% per annum.

- Expenses charged to asset share are as per the actual expenses incurred by the Company and are charged to different lines of businesses basis Axis Max Life’s Expense allocation policy, approved by the Board from time to time. Hence, the expense allocation to participating business could vary depending on multiple factors like type and volume of business, distribution channel mix etc.

- Actual Claim payouts are deducted from the Asset Share. These claims include death, surrender and maturity payouts.

- Policyholder Bonuses are usually declared annually, reflecting the performance of the participating fund. Based on the bonus option available, these bonuses get paid in cash each year, or accumulate under the reversionary bonus option, and may get paid out when policy matures or exits (death or surrender).

Bonus earning capacity is determined by comparing the asset share with expected future cash flows at the product level. Actual performance is regularly monitored and compared with future expectations, and accordingly the bonus rates are reviewed on annual basis.

Policyholders may refer to their past annual bonus statements to review the bonuses credited against their contracts.

In addition, Axis Max Life Insurance has a surplus of ₹4,496 crore in the participating fund as of March 31, 2026. This surplus or sometimes known as Fund for Future Appropriation (FFA) is maintained primarily to ensure the financial resilience of the participating fund.

The customer’s Internal Rate of Return (IRR) at maturity is expected to align closely with the IRRs illustrated at the time of sale. For reference, the chart below presents the fund returns achieved over the past five years.

Disclaimers:

Past performance of the participating fund is not indicative of future returns.

Investment returns achieved by the participating fund are not the same as bonus rates declared on policies.

All information provided is based on data available as of March 31, 2026. Figures and assumptions may be revised in future disclosures.