Individual

Individual

Get ₹1 Cr Term Plan @ <del>₹700</del> <span style="color:#ffc31f;">₹595/Month<sup>@7</sup></span>

15% Discount<sup>3</sup>

<b>SAVE TAX</b><b>Up to Rs.46,800<sup>~#</sup></b><b>99.8%</b> Claims Paid Ratio^<b>3 hours</b> Instaclaim^*Check PremiumInvest ₹10K/M & <br>Get ₹3.92Cr.<sup>*7</sup>

Valid till 20<sup>th</sup> August

<span class="text-white dark:text-white font-bold text-12px"> Extended Fund Offer </span><span style="color:#000000;font-size:10px;">Sector Leaders Opportunities Fund</span> <b>0%</b> GST Benefit<b>Free</b> Fund Switches View PlansInvest $1K/M & Get $3.64M<sup>&1</sup>

<span class="text-white dark:text-white font-bold text-12px"> NFO Live </span>Global Innovation Leaders Fund Tax Free <b>Corpus</b>Free <b>Fund Switches</b>View PlansGet ₹3 Cr Term Plan @ <del>₹1544</del> <span style="color:#ffc31f;">₹1312/Month<sup>@6</sup></span>

15% Discount

<b>SAVE TAX</b><b>Up to Rs.46,800<sup>~#</sup></b><b>99.8%</b> Claims Paid Ratio^<b>3 hours</b> Instaclaim^*Check PremiumInvest ₹15K/M & <br>Get ₹5.98Cr.<sup>*7</sup>

Valid till 20<sup>th</sup> August

<span class="text-white dark:text-white font-bold text-12px"> Extended Fund Offer </span><span style="color:#000000;font-size:10px;"> Sector Leaders Opportunities Fund</span><b>0%</b> GST Benefit<b>Free</b> Fund SwitchesView PlansInsurance Policies for Every Need

Why 3 Crore+ Indians

Choose Axis Max Life ?

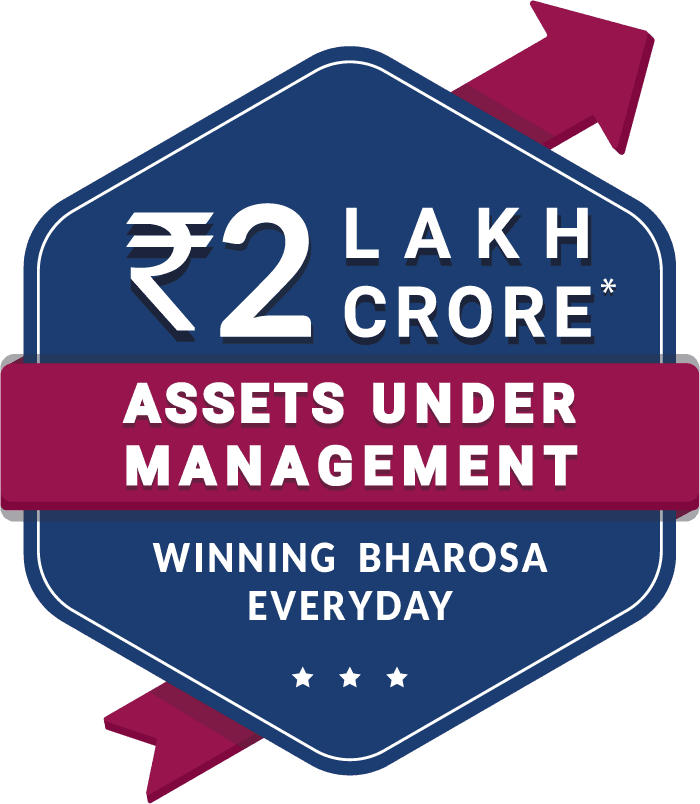

Axis Max Life Insurance Limited (formerly known as Max Life Insurance Co. Ltd.) is a Joint Venture between Max Financial Services Limited (“MFSL”) and Axis Bank Limited. Axis Max Life Insurance offers comprehensive protection and long-term savings life insurance solutions through its multi-channel distribution, including agency and third-party distribution partners. Axis Max Life Insurance has built its operations over two decades through a need-based sales process, a customer-centric approach to engagement and service delivery and trained human capital. As per the annual audited financials for FY2024-25, Axis Max Life Insurance has achieved a gross written premium of ₹33,223 Cr. Here are some of the numbers that speak about our accomplishments.99.8% Death Claims Paid Ratio

Source : Individual Death Claims Paid Ratio as per audited financials for FY 2025-26)

₹2,191,857 Crore Sum Assured

In force (individual) (Source : Axis Max Life Public Disclosure, FY 2024-25)

₹2 Lakh Crore Assets Under Management

(Source : As per financials closed on 30th June 2026)

405 Branch - Touchpoints of Trust

Axis Max Life Presence (Source : As reported to IRDAI, FY 2024-25)Life Insurance

For the insurance policy to be enforceable and life insurance quotes to be accurate, your application must accurately disclose your current and past health conditions. Also, you need to pay a single premium or regular premiums as chosen when buying life insurance. You can estimate the life insurance quotes for your financial profile by using the insurance calculators.

Simplifying Life Insurance For you

Life Insurance Purchase

You need to spend maximum time deciding on buying the most suitable life insurance plan at this stage. The life insurance quotes for your financial profile will help you make the decision. Although the best life insurance policies offer the flexibility to choose the benefits, the ultimate choice lies in your hands.

Hence, you must consider various factors, like plan tenure, premium, riders, and, most importantly, the reason to buy life insurance and find the life insurance quotes. You can then buy the plan online or offline as per your preference.

Premium Payment

As per the life insurance contract, the insurers promise to pay a pre-decided amount to the life insured or policy nominee provided the insured pays the premium without fail. In other words, all the benefits that you can get under a life insurance policy are based on the timely premium payment.

- To calculate premiums for term insurance use Term Insurance Calculator.

- To calculate premiums for investment plans use Investment Calculator.

Hence, it is advisable to choose a premium that you can easily pay on time along with other financial liabilities. Your life insurance quotes will allow you to speculate on the premium costs in the coming years.

Claim Filing

The last stage of a life insurance plan is related to filing for a claim to get the expected insurance policy benefits.

In case of your unfortunate demise, the nominee will receive the sum assured as defined in the contract. To receive it, the nominee has to submit a claim form along with various documents. Upon verification of claim, the insurance company releases the benefit to the nominee.

For life insurance plans with a return of premium option, the insured gets the total of all premiums paid back if insured person survives the policy term, which can be used to achieve several life goals.

As a contract between an individual (the policyholder) and an insurance company, a life insurance policy offers the nominee the death benefit in case of the death of the policyholder. The following are the key benefits of having a life insurance policy:

The following are the benefits of life insurance:

Provides Financial Security for Your Family

Life insurance ensures that your loved ones are financially protected in case of your untimely death. The payout helps your family cover living expenses, pay off debts, and maintain their lifestyle even in your absence.

Acts as a Long-Term Savings Tool

Certain life insurance plans combine protection with savings, allowing you to build a financial corpus over time. This can serve as a stable source of income during retirement or for future needs.

Supports Your Children’s Future

It can support the education, marriage, or other major milestones of your children. So, it ensures that your financial difficulties do not affect their future ambitions.

Provides Income during Health-Related Setbacks

Some insurance policies offer financial support if your earning capacity decreases due to a severe illness or accident. This benefit can help you manage treatment costs and household expenses during recovery.

Prepares You for Unexpected Expenses

Life insurance assists you in managing unexpected financial requirements or emergencies. It provides liquidity and financial stability, allowing you to manage lifestyle expenses or sudden obligations without stress.

Provides a Source of Income for Your Family:

If you have dependents who rely on your income, a life insurance policy can help ensure that they have a source of financial support even if you're no longer around.

Can be Used as an Investment Tool:

Certain types of life insurance policies, such as whole life insurance, accumulate cash value over the policy term, which you can use as an investment tool for your future financial goals.

Offers Tax Benefits:

Life insurance death benefits are generally tax-free, and the premiums you pay for the policy may also be tax-deductible in some circumstances.

Can Help Cover Debts and Loans:

If you have outstanding debts or a loan, a life insurance policy can provide the funds to pay these off so that your loved ones are not left with these financial obligations.

Can Provide Peace of Mind:

Knowing that you have life insurance in place can bring peace of mind, as you can be confident that your loved ones will be financially taken care of in the event of your death.

Following are the most important types of life insurance available in India:

| Type of Life Insurance Policy | Key Features | Ideal For | Maturity Benefit |

|---|---|---|---|

| Term Insurance | Offers life cover for a chosen duration. Pays a benefit to dependents in case of death or total and permanent disability if the insurance policy includes that feature. No payout is usually made if the insured outlives the term. | Individuals seeking affordable protection for a fixed period. | Not applicable |

| Whole Life Insurance | Provides cover throughout one’s lifetime. Ensures a guaranteed death benefit, helping families stay financially secure in the long run. It can also help create a financial legacy for heirs. | People who want lifelong protection and wish to leave an inheritance. | Yes |

| Endowment Policy | Merges saving and insurance. Pays the sum assured to nominees in the event of death or disability of the insured within the policy period. In case the policyholder lives until the end of the term, the maturity value is given out. | Those who want disciplined savings along with life cover. | Yes |

| Money Back or Cash Back Plan | Survival benefits are paid as a part of the sum assured at regular intervals. The remaining amount is paid at maturity. The life cover continues for the full sum assured throughout the term, regardless of payouts already made. | People who prefer periodic returns rather than waiting till the end of the policy. | Yes |

| Children Policies | Policies made to secure the future of the child. Benefits can be designed in a manner to make funds available when there are major milestones. Many plans waive future premiums if the parent passes away during the term, allowing the policy to continue. | Parents planning long-term financial support for their child’s education or life milestones. | Yes |

| Annuity Pension Plans | Converts retirement savings into a regular income stream. Gives financial security even after retirement. | Professionals and retirees seeking guaranteed post-retirement income. | Yes |

| Unit Linked Insurance Plans (ULIPs) | Blend investment with life cover. Allow the policyholder to choose funds and switch between them. Market performance affects the value of units invested. Charges such as fund management fees apply. Investment risk lies with the policyholder. | Investors who are comfortable with market-linked returns and want insurance and growth potential. | Depends on the performance of the fund |

Let's understand all the types of life insurance briefly below.

Term Insurance

It is the simplest types of life insurance that provides financial safety to the life insureds family in case of the untimely demise. Depending on your income and liabilities, you can select an adequate sum assured under this type of life insurance plan to safeguard the financial interest of your loved ones.

ULIP

A Unit Linked Insurance Plan or ULIP is a unique form of life insurance. It provides life cover while also allowing you to invest money in market-linked instruments. By investing in ULIPs, you get the benefits of market linked returns over the long term, life cover, income tax savings, and flexibility to switch between funds. The life insurance quotes will enable you to determine the amount required for financial security and investment purposes, so that you can divide it efficiently.

Retirement Plans

These plans are insurance policies that provide financial security for your retirement days. These life insurance plans help you invest money during the working years and create a corpus that you can use as a whole or in parts to fund your retired life. You can think of investing in retirement plans as a disciplined way to plan for the golden years of life.

Child Plans

Child insurance plans, commonly known as saving life insurance plans, are designed to help you secure your child's future. Along with life cover, your child receives the benefit of pay-outs at different milestones during the educational journey under these life insurance plans. Investing in child plans shields your child's future against unfortunate events like death or critical illnesses

Savings and Income Plans

As life insurance products, these plans can help you instill the habit of disciplined savings to ensure steady returns in the form of monthly income or a lumpsum amount. Alongside, these life insurance plans provide various other benefits, including death benefits, tax benefits, terminal illness benefits, to name a few. Check the life insurance quotes and details before making investment decisions, so you can allocate your money in the right places

Group Insurance Plans

These life insurance plans are meant for organizations or groups to provide life cover to the employees or group members, respectively. Through group insurance plans, the employers tend to take care of the financial security of their employees’ family, thus motivating them to work harder to maintain high-performing businesses. Keeping this cover in mind, you can check the life insurance quotes for additional financial security for your loved ones.

Whole Life Plan

A whole life plan is type of a life insurance plan which provides life cover benefit till the age 100 years. Many consider this as a term plan with a policy term that extends for the entire life of the insured individual. So, in this term plan variant, the death benefit is paid out to the nominee if the insured individual dies at any time before attaining the age of 100 years. A whole life plan typically does not offer maturity benefit to the insured individual if they attain the age of 100 years.

Endowment Plan

An endowment plan is a type of life insurance plan that combines the benefit of life cover along with long-term savings benefits. So primarily, an endowment plan ensures that the policy beneficiary received additional protection in the case of the insured individual’s untimely demise while the plan is in force. Additionally, this life insurance plan also provides maturity benefits through accrued savings if the insured individual survives the policy term.

Annuity Plans

Annuity or retirement plans help individuals accumulate long-term wealth. These plans provide financial stability after retirement.

Policyholders pay premiums regularly during the policy term. Insurers accumulate these premiums to build a retirement corpus.

The plan provides a lump-sum payout at maturity. It may also offer regular annuity payments. Policyholders choose the payout option based on their preferences.

Some annuity plans guarantee payouts to nominees. Insurers pay the nominee if the policyholder dies during the term.

Money Back Policy

A money-back policy is a life insurance policy. It pays policyholders fixed survival benefits at predefined intervals.

The insurer returns a percentage of the sum assured periodically. If the policyholder survives the term, the insurer pays maturity benefits. The insurer usually pays the remaining sum assured with accrued bonuses.

If the policyholder dies during the policy term, the nominees receive benefits. The insurer pays the full sum assured regardless of earlier payouts in most traditional money-back policies.

Participating Life Insurance Plans

Participating life insurance plans share company profits with policyholders. Insurers distribute these profits as dividends or annual bonuses. Insurers usually declare bonuses on an annual basis. The bonus amount depends on the insurer’s overall yearly performance.

Policyholders can use bonuses to increase overall returns. They may also use payouts to pay due premiums. Policyholders can deposit bonuses with the insurer for interest income.

Insurers pay these bonuses in addition to maturity benefits. Insurers also add bonuses to death benefits under the insurance policy

Many investors tend to make a common mistake of investing in instruments without factoring their entire financial picture – the equity they have built-in their home, existing loans, and other liabilities. Ideally, every asset and investment you own should factor into your risk-reward equation.

Getting your life insurance plan at an appropriate stage in life allows you to take more risk when it comes to securing your life and making sure that you provision a significantly large financial corpus (in the form of insurance coverage) as backup against contingencies, while continuing to invest for other life goals. Moreover, with a life insurance plan in your pocket, you can be sure that even if something happens to you, your family will not have to deal with a financial crisis at any time during their lives.

Planning with life insurance plans will help your family stay financially protected, serving as a safety net that will prove useful in case of an eventuality. Also, the insurance coverage will augment the total accumulated value of your investments, making sure that your loved ones continue to have a lifestyle that you intended for them, even if you are not there with them.

When you buy life insurance, you buy protection plan that’s carefully designed to protect your family from future mishaps. If something unfortunate happens to you, your insurer makes sure that the payout is paid timely to your chosen nominee.

This life insurance payout helps your kids, spouse, parents manage everyday expenses and other financial responsibilities without depending on others or drowning in debt.

The process of buying a life insurance starts by choosing the right type of policy. How do you define the right insurance policy? Well, it’s simple. You choose the sum assured, policy duration, premium amount, and optional riders that suit your lifestyle and needs.

It’s recommended to factor in family size, any current loans, and long-term financial commitments while deciding life insurance coverage.

After selecting a plan and completing an application, you might have to go through medical tests to assess health risk appropriately. Your accurate premium is decided on the basis of your age, lifestyle, profession, and medical history.

Upon approval, you pay the first premium and your policy gets activated. You receive a insurance policy document, usually online, sometimes offline too, which has policy conditions, benefits, and exclusions in simple, clear language.

You have to pay premiums on time to keep the policy active. A lapsed policy puts your family’s future at risk because the insurer cannot provide benefits if coverage is inactive. Most insurers also offer grace periods to help policyholders maintain continuity.

Now your job is to keep paying the premiums on a monthly, quarterly, of annual basis so that your insurance policy doesn’t get lapsed.

In case of unfortunate event, during the active policy period, your nominee can file a claim with the insurer. The claim process generally involves submitting the claim form, death certificate, and identity documents.

Insurers review the claim and release the payout after following standard verification procedures. This ensures your family receives timely support without unnecessary stress. With Axis Max Life Insurance’s Insta Claim facility, claim is paid within a few hours, without any hassle.

The most important reason to consider a life insurance is to provide long-term financial protection to your family when they need it the most.

When you look at the dynamics of most Indian families, a single income supports multiple dependents. The sudden loss of that income can cause financial stress and put your kids, spouse, and parents in a tough spot.

Life insurance absorbs that shock by offering a guaranteed payout to your family in case of your unfortunate demise.

With this amount, it will be easy for them to manage daily expenses, lifestyle needs, and future goals. It ensures that they have their financial independence rather than depending on relatives or loans.

Life insurance is extremely crucial for you if you have long-term responsibilities. Your long-term responsibilities include children’s education, your parents’ medical bills, or loans taken for a home or any other needs.

Life insurance encourages disciplined saving through regular premium payments. There are some types of term life insurance plans that offer maturity benefits that help build wealth over time.

If you fall under the old tax regime, your life insurance premiums may qualify for tax benefits, helping you save more while securing your family’s future.

An important thing to keep in mind is that young and healthy individuals enjoy lower premiums and wider plan options.

You should buy life insurance because it provides certainty and protection in situations where your family may have to go through financial stress. Buying an insurance policy ensures your dependents receive financial support if something unexpected happens to you.

This support helps them manage essential expenses without affecting their long-term goals. In Indian households, financial responsibilities often extend across generations.

You may be supporting parents, spouse, children, or even siblings based on family expectations. Life insurance ensures these responsibilities continue without disruption.

Buying life insurance ensures your family maintains their current lifestyle. Your income helps pay for rent, EMIs, school fees, and daily expenses, which cannot stop suddenly. A life insurance payout replaces this income and reduces financial shock.

One major reason to buy life insurance is protection from long-term liabilities. Many people take home loans, education loans, or business loans to fulfil family needs. If something happens to you, these obligations can put your dependents under immense pressure. Life insurance ensures your family does not lose assets or face pressure.

At its core, life insurance is a financial benefit for possible contingencies linked to human life. These include death, disability, or retirement. When these contingencies occur, they result in loss of income for the household. It is where a life insurance plan works to benefit you and your family.

Under a life insurance plan, a monetary sum is offered as per life insurance plan opted to help cope up with the loss of income in the future years. Depending on your life insurance quotes, it can relieve a significant amount of financial burden. Hence, you should buy life insurance:

- To ensure financial support to your immediate family after you

- To finance your child's education plans

- To get a steady source of income in life

- To get insurance benefits in case your earnings are impacted due to a critical illness

Having life insurance gives you more than just a life cover. It also helps create wealth over the long term for you and your loved ones. Most importantly, life insurance gives peace of mind that your family will live life comfortably, should anything happen to you.

People who face more financial uncertainty in the future are likely to buy life insurance. These people are more aware of the need for financial protection for their families, which makes them interested in getting sufficient coverage.

For newly married people

After you have just tied the knot with a better half, you get the responsibility to plan for his/her well-being as well. Your life insurance quotes as a single person and married person will vary as you will have increased financial obligations. Along with the plans that you have already made for the life ahead, it always helps to prepare for the future with a life insurance plan.

For young parents

As a young parent, you can feel immense joy all around. Alongside your spouse, you now have another life to care for. With a life insurance plan, you can plan for your child's future in terms of education, marriage, and many others. The life insurance quotes when you buy a plan for your child's future will account for these factors. They will ensure that your kids’ dreams get fulfilled as planned.

For individuals with financial liabilities

Along with a growing family, the liabilities grow as well. To accommodate your loved ones, you buy a bigger home or buy a dream car that they all love, which gets added to your liabilities. Purchasing a life insurance plan for your loved ones ensures that your loved ones can shoulder these liabilities easily, if you have the right life insurance quotes.

For people nearing retirement

Retirement planning is something that you should not take lightly, regardless of your current income. By investing in a life insurance plan, you can build a corpus for your twilight years and live life without facing financial dependence. You can also plan to receive a steady income during the retired life by getting reliable life insurance quotes, at the right stage in life.

Smokers

Smokers are among the most likely people to consider life insurance because of the health risks that come with smoking exposure. Regular smoking is linked to lung disease, heart-related issues, cancer etc, which can reduce life expectancy. This increased risk encourages smokers to secure financial protection for their families.

Premiums are usually higher for smokers, but people still get life insurance to ensure their family remains protected.

Disabled Individuals

Disabled people may get life insurance to offer long-term financial security to their families. Living with a disability can result in uncertainty regarding income and future medical expenses, making financial planning important.

Life insurance makes sure that family members are taken care of during an untimely death. For such individuals, there is usually stricter underwriting or higher premiums, but there are also customized plans they can go for.

People with Pre-existing (PED) Diseases

People with PEDs are highly motivated to buy life insurance. Conditions such as diabetes, heart disease etc can increase the chances of future health complications, encouraging people to secure financial protection early.

Although premiums are usually higher and policy options are limited, many insurance companies now provide specialized plans for such people. Life insurance allows them to ensure their family’s financial needs are met.

Life insurance helps you to take care of family's financial security in future. Before applying you should keep the following documents ready at your end to speed up the processing:

- Address proof: Aadhar, passport, driving license

- Income proof: Salary slips, bank statement, ITR

- Identity proof: PAN card, passport, driving license

- Medical history: Any relevant medical records

- Photograph: Might asked to provide a passport size

Life insurance is an important financial commitment. However, many people think that the process of buying an insurance plan India is too complicated, but the reality is somewhat opposite. You can follow the instructions below and get an insurance policy in no time:

- Firstly, you need to identify your goals and select a preferred plan. For example, if you have a home loan and you want to protect your family from the financial burden of the loan, in case of life loss, you should select an Axis Max Life Term Insurance Plan.

- After that, decide how much you can invest per month or year given your annual net income with a help of premium calculators.

- Add riders (if needed) such as accidental death benefit to avoid any sudden financial liability later.

- Next, complete the application form.

- Pay the premium. You will get choice of payment options if you opt for online payment mode.

- Appear for medical examination, if your policy mandates you to do so.

- After that the policy will be processed for background checks and verifications. Once completed, the policy will be issued and shared on your registered email address.

Almost all insurance companies in India have made life insurance plans available online, and a rising number of people are choosing the online mode. If you are still confused about what method you should choose, then here is a rundown of some advantages of buying a life insurance plan online:

- Online life insurance is less expensive than offline mode because insurance companies are not required to pay commissions on plans offered online.

- By using online platforms, you can readily compare various products from all of the top insurers.

- When searching for life insurance online, no one is forcing or pressuring you to choose a specific policy. So, you are less likely to take biased decisions.

- There are online platforms that allow you to browse, compare, and purchase a policy at any time in order to make your application process easy and informed.

The ideal amount of life insurance coverage varies for each individual and depends on several personal and financial factors, including:

Number of Dependents

The more individuals depend on your salary, the greater the coverage you are going to need to provide them with financial security.

For example, if you have a family of 4 and are the sole earning member, you must select a sum assured amount which is 15 to 20 times your annual income. Say a ₹2 crore life insurance policy if you are earning 10 Lacs annually. This helps ensure that there is adequate financial coverage for all your dependants.Desired Lifestyle for Your Family

Take into account the quality of life you would wish your family to live in if you’re not around.

Children’s Education Expenses

Consider future education expenditure and other key financial objectives of your children.

Investment and Financial Goals

Your coverage must be in line with your long-term financial strategies, such as savings or wealth-building requirements.

Prepares You for Unexpected Expenses

Life insurance assists you in managing unexpected financial requirements or emergencies. It provides liquidity and financial stability, allowing you to manage lifestyle expenses or sudden obligations without stress.

Budget and Affordability

pChoose an insurance policy that provides adequate protection without straining your current finances. For instance, getting life insurance early in your career can be a smart move. Purchasing a term plan in your 20s helps you lock in much lower premiums for a long period. If you are a 25-year-old non-smoker, you can get a ₹1 crore policy by contributing just ₹7,000 to ₹10,000 per year (approximately basis T&C appliable).

It gives you affordable protection now while ensuring your loved ones are secure if new obligations arise later, such as family support or a loan repayment.We all know that life insurance can give us a much-needed sense of security, but can we afford the insurance premium? If you are wondering what affects your life insurance premium in the first place, then check the below listed factors, before you commit:

- Your Age: Generally, younger individuals are subjected to lower premiums. As age increases, the risk of insurance providers rises and resulting in higher premiums.

- Policy Term: Long-term policies come with higher premiums due to the extended coverage period.

- Sum Assured: A higher sum assured corresponds to a higher life insurance premium. The reason for this is that a higher payout raises the risk for the insurer, which impacts the premium price.

- Medical History: Life insurance companies in India may request a medical examination to assess overall health. Existing health conditions at the time of examination can result in higher premiums.

- Occupation: Riskier occupations like mining work lead to higher premiums, reflecting the increased likelihood of potential claims.

Understanding the insurance requirements is essential when selecting the correct life insurance plan. Hence, to make an informed decision, follow these steps and find the best life insurance plan that best suits your needs:

- Determine Your Insurance Needs: In order to select the right life insurance, amount of coverage, and policy term, you have to start by figuring out your family's financial requirements, future goals, and current lifestyle.

- Compare Plans and Premiums: Select a life insurance policy that offers maximum value at a premium that completely fits your budget. For comparison, you can use take help of a life insurance calculator and check different plans.

- Consider Your Budget: Age, health, and policy type can influence the cost, so it's important to select a premium amount that you can afford on a monthly or yearly basis.

- Check for Riders: Life insurance riders add a great value in your new/existing policy as they enhance your coverage in unfortunate events like accident or illness. So, take your time to consider your needs before deciding which ones to select.

- Check the Claim Settlement Ratio (CSR): Only consider insurance providers such as Axis Max Life Insurance that show a demonstrated history of consistent high claim settlement ratio over at least last 3 years while choosing an insurance policy India.

- Check Company Reputation: Before selecting an insurance company, you must research its financial stability, claim settlement ratio and customer service record. It ensures that your insurance needs will be met in an efficient manner.

Axis Max Life Insurance is known for its strong customer-centric approach and financial stability, which offers various insurance plans, including savings, protection, and pensions. So, if you are wondering why you should choose Axis Max Life as your life insurance partner, here are some top reasons that help you to know more about it:

- Axis Max Life Insurance is a joint venture between Axis Bank Ltd. and Max Financial Services Ltd. So, it brings double trust of two large Indian companies.

- With a claim settlement ratio (CSR) of 99.8%^, Axis Max Life offers assurance to insurance buyers in case of any unfortunate development in life.

- Axis Max Life focuses on customer satisfaction and ensures smooth customer buying journeys.

- The company provides a very understandable claim settlement process in case the nominee files the claim.

- The company is committed to an excellent customer support service to insurance buyers.

Axis Bank + Max Life Insurance = Axis Max Life Insurance = Double The Bharosa!

- 20+ Years of Trust in Insurance with Axis Max Life Insurance

- Proven Track Record with Over ₹2,191,857 Sum Assured and 201% Solvency Ratio.

- Joint Venture with Axis Bank – Enhanced Customer Access

- Consistent Death Claim Paid Ratio Over 99% mark for more than 5 years

On December 13, 2024, Max Life Insurance rebranded itself as Axis Max Life Insurance. This rebranding is a significant milestone in the evolution of Axis Max Life Insurance and strengthens the company’s association with Axis Bank, which has been a key partner in the life insurance space.Axis Max Life Insurance Term Plans

- Axis Max Life Smart Term Plan Plus: This is a Non-Linked, Non-Participating Individual Pure Risk Life Insurance Plan that offers unmatched flexibility to help safeguard your family's financial future, even in the face of unforeseen circumstances.

- Axis Max Life Smart Secure Plus Plan: This Non-Linked Non-Participating Individual Pure Risk Life Insurance Plan provides the insured with not just life cover benefit but also includes an in-built cover for terminal illness and the option of availing returns of Premium.

- Axis Max Life Smart Total Elite Protection Term Plan: This Non-Linked, Non-Participating Individual Pure Risk Life Insurance Plan offers comprehensive and customisable protection solution at an affordable premium so that your family's lifestyle can be maintained even in your absence.

Axis Max Life Insurance Savings Plans

- Axis Max Life Capital Guarantee Solution: This savings solution from Axis Max Life Insurance combines the benefit of guaranteed returns of Axis Max Life Insurance Smart Wealth Advantage Guarantee Plan with benefit of the market-linked returns of Axis Max Life Insurance Online Savings Plan in a single package.

- Axis Max Life Smart Fixed-return Digital Plan: This online-only solution from Axis Max Life Insurance allows you to lock-in interest rates at policy inception. This way you can grow your wealth and get tax-free returns without worrying about changing market conditions.

- Axis Max Life Smart Wealth Advantage Guarantee Plan aka SWAG Plan: This is a Non-Linked Non-Participating Individual Life Insurance Savings Plan. Axis Max life SWAG Plan offers guaranteed returns along with life cover benefit, which is ideal for long-term wealth building and tax savings.

Axis Max Life Insurance ULIP Plans

- Axis Max Life Flexi Wealth Advantage Plan: This Unit Linked Non-Participating Individual Life Insurance Plan from Axis Max Life Insurance offers various unique features to policyholders such as return of all charges1, guaranteed loyalty additions to enhance your fund value~*, auto-debit boosters, smart withdrawals and more.

- Axis Max Life Smart Term with Additional Returns ULIP: This Unit Linked Non Participating Individual Life Insurance Plan from Axis Max Life Insurance features the benefit of high sum assured with market-linked capital appreciation. This highly customisable plan features key benefits like unlimited free fund switches, emergency withdrawal options and return of charges.

Axis Max Life Online Savings Plan:

- This ULIP plan from Axis Max Life Insurance helps maximise capital appreciation with unique features such as nil administration and allocation charges. With multiple funds to choose from this plan can fulfill the needs of investors with various risk profiles and ensure financial security of loved ones with in-built life cover benefit.

Axis Max Life Insurance Child Plans

- Axis Max Life Shiksha Plus Super Plan: This is a Unit-Linked Non-Participating Individual Life Insurance Plan from Axis Max Life Insurance can help fund your child's education cost and future. With a policy term of 15 years to 25 years and guaranteed loyalty addition, this is a smart way to save for your child's future higher education expenses.

Axis Max Life Insurance Retirement & Pension Plans

- Axis Max Life Guaranteed Lifetime Income Plan: This is a Non Linked Non-Participating Individual General Annuity Savings Plan from Axis Max Life Insurance. It offers policyholders with risk-free life-long income so that they can enjoy their golden years without financial stress

- Axis Max Life Smart Guaranteed Pension Plan: This is a Non-linked, Non-Participating, Single Premium Individual/Group General Savings Annuity Plan offered by Axis Max Life Insurance. This retirement solution offers customisations such as joint-life to ensure payouts to the spouse after death of the primary annuitant and death benefit in the form of a lump sum payout of the premium amount to the nominee

- Axis Max Life Smart Wealth Annuity Guaranteed Pension Plan: This retirement solution from Axis Max Life Insurance is a Non-Linked, Non-Participating Individual/Group General Annuity Savings Plan. The plan offers multiple customization options to ensure that your post-retirement lifelong income is aligned with your unique lifestyle needs and keeps pace with rising inflation.

Axis Max Life Insurance NRI Plans

- Term Plan with Health Insurance Benefits from Axis Max Life Insurance: Secure Earnings Wellness Advantage Plan: Also known as Axis Max Life SEWA. this solution is a Non-Linked, Non-Participating Individual Life Insurance Savings Plan that combines a range of wellness benefits with savings and protection. This can help manage health costs and fulfill financial goals during your lifetime while ensuring the financial protection of your loved ones after your death.

A claim refers to an official request filled with your insurance company claiming a payout an eligible event in case of policyholder's demise/maturity. To file a life insurance claim, here are the steps you have to follow:

- Step 1: As a first step, the nominee should formally inform their insurance company if the policyholder dies.

- Step 2: Next, the nominee has to fill in the claim form that the insurance company provides along with any supporting documents (if any).

- Step 3: After that, the company will appoint an agent who verify if the policyholder dies and do further authenticity checks.

- Step 4: After confirmation from the agent, the insurance company will inform you the time it will take to process and make the payment to the beneficiary.

Axis Max Life Insurance provides flexibility in how your family receives the policy benefits after your passing. You can select a payout option based on what best fits your family’s financial needs and comfort.

The available options include:Lump Sum Payout

In this option, the nominee gets the whole sum assured amount in one payment in case of the death of the insured individual within the policy period. This offers instant access to money and assists the family to meet huge financial obligations, including repaying loans, school fees or family bills.

Acts as a Long-Term Savings Tool

Certain life insurance plans combine protection with savings, allowing you to build a financial corpus over time. This can serve as a stable source of income during retirement or for future needs.

Lump Sum + Monthly Income Payout

Under this arrangement, the nominee gets the sum assured amount as a one-time payment, along with fixed monthly payments over a certain period of time (selected by the policyholder at the time of purchase).

This guarantees the immediate monetary relief and also a continuous flow of income to cover your daily living costs, thereby providing your family with monetary stability in the long run.

Life insurance claims are classified into three categories, i.e. death claims, rider claims, and maturity claims. To get life insurance claims settled easily, you have to submit the following relevant documents to the insurer:

- Original Policy documents

- Original/attested copy of death certificate issued by local municipal authority

- Death claim application form (Form A)

- NEFT mandate form attested by bank authorities along with a cancelled cheque or bank account passbook

- Nominee's photo identity proof such as copy of Passport, PAN card, Voter identity card, Aadhar (UID) card, etc.

- Current Address proof of the claimant. (Any one of the following: Aadhar Card, Valid Passport or Driver's License, Voters ID are considered as proofs)

- Signed copy of PAN card / Form 60 of the claimant

- Employer certificate with complete leave records- Form E

- ITR for last 3 years’ / GST certificate in case of Self-employed

- Other life / health insurance details with claim history details

- Bank statement of last 2 years of the Life Assured

- Body transfer certificate / Embassy documents / Post Mortem report whichever applicable in case of death in foreign country

- Complete Passport copy in case of death in foreign country

- Medical booklet / CGHS card details in case of Defence and Central Govt personnel

- Attending physician's statement (Form 'C')

- Medical records (admission notes, discharge/death summary, test reports, etc.) of current and /or any previous admissions

Medical/Natural death:

- Attending physician's statement (Form 'C')

- Medical records (admission notes, discharge/death summary, test reports, etc.)

- Medical booklet / CGHS card details in case of Defence and Central Govt personnel

Accidental/Unnatural death:

- Copy of the First Information Report (FIR) or Panchanama/Police complaint

- Copy of Post Mortem report (PMR)/Autopsy and Viscera report

- Copy of the Final Police Investigation report (FPIR)/Charge sheet

- News Paper Article, if any

- Driving License

Life insurance is not only a financial product; it is a safety blanket for your loved ones that provides a lump sum of money to your family if you are no longer with them. Having a detailed understanding of life insurance is critical. Therefore, to make this easier to comprehend, sharing a quick refresher on some of the most common life insurance terms:1- Accident: An accident is an unplanned circumstance that occurs suddenly, typically resulting in unintended.

2- Agent: The agent of the insurance company sells its products and works as is an intermediary between the policyholder and an insurer.

3- Annual premium: The amount that an individual or entity has to pay annually to an insurance company for the policy opted.

4- Cash value: The investment or saving component of permanent life insurance that grows over time and under some specific circumstances, can be accessed by the policyholder.

5- Beneficiary: In the event of policyholder death, the individual or entity will get the benefits of the insurance policy or bank account.

6- Death benefit: If the insured person passes away, then the insurer pays your nominee(s) as per the agreement in the insurance policy

7- Free-look period: This is the time during which you may cancel the insurance policy without losing the premium paid.

8- Grace period: This is a specified time period that allows the policyholder or insured to make the premium payment that has been delayed. If you do not pay the premium within the grace period (15 days for monthly premium plans and 30 days for other plans), your term insurance policy will expire.

9- Maturity date: It takes place when a life insurance policy expires and the policyholder gets the cash value or other agreed-upon advantages.

10- Limited premium: It is a cost that can only be paid for a specific, time-limited period. Policies coming with limited premium option helps you to save money.

11- Term insurance premium: This is the amount of money that the insurance company charges in return for the coverage offered under a term insurance plan.

12- Policy term: The time frame of the life insurance coverage is known as the policy term. It is the period of time, expressed in years, that the policyholder decides from the start of the life insurance plan until its maturity.

13- Claim: It’s a formal request raised by policyholder/beneficiary/nominee to the insurance company for the payment of benefits of the policy.

14- Riders: Riders are additional benefits that can be separately purchased to get different kinds of coverage under an insurance plan, such as cover for accidental death, critical illness, or total or partial disability. All you have to do is pay an additional nominal premium. If you wish to opt for it

15- Joint life insurance: This life insurance plan provides coverage to two people. It's beneficial for a spouse who wants to insure both of their lives under a single policy.

16- Nominee: The person designated by the policy owner to receive the benefits in case of life assured dies. Spouse or children are made nominee by policyholders.

17- Maturity: Period/point of time after which the policyholder/beneficiary gets the promised benefits under the life insurance.

18: Reinstatement: The process of reactivating a lapsed insurance policy due to non-payment of premiums.

19- Lapsed Policy: A deactivated/expired policy due to failure in premium payment.

20- Policyholder: The individual/entity who owns the insurance policy and supposed to receive the benefits under agreement.

21- Life Assured: The individual/entity for whom the insurance policy provides life coverage.

22- Claim Settlement Ratio (CSR): No. of claim settled against raised claims by a life insurance provider in year. Always look for insurers with highest claim settlement ratio.

23: Quote: An insurance quote denotes the estimate of price you are supposed to pay for your policy.

Buying life insurance in India can be a smart choice for NRIs due to the following reasons:

- Financial Protection for FamilyThe need to support loved ones in India is one of the major priorities of many NRIs. A life insurance policy provides financial security to your dependents in the event of your passing, helping them manage living costs, repay loans, and maintain their quality of life. The death benefit guarantees that the financial future of your family is not lost just because your income is gone.

- Simplified Estate and Wealth PlanningNRIs often hold assets across different countries, which can make estate distribution complicated. Life insurance makes transferring wealth to the heirs easy, as it provides them with quick access to the funds without the tedious legal processes. Moreover, the death benefit is usually tax-free, which makes passing on wealth an efficient and tax-saving instrument

- Helps Achieve Long-Term Financial GoalsLife insurance can also be a structured savings plan towards your financial milestones. Whether you are planning your child’s education, purchasing property in India, or preparing for retirement, various policies offer maturity benefits that can be aligned with your long-term goals.

- Offers Tax AdvantagesLife insurance is also beneficial from a tax planning perspective. Premiums paid towards your policy may qualify for deductions under [Section 80C ](/blog/tax-savings/section-80c)of the Indian Income Tax Act.

- Protects Against Currency FluctuationsExchange rate volatility can impact the value of your overseas earnings and investments. By investing in a life insurance policy denominated in Indian Rupees, NRIs can protect a portion of their wealth from currency risk and ensure stable financial returns in the long run.

- Peace of Mind While Living AbroadLife abroad can be unpredictable, and being far from family often adds emotional strain. A life insurance policy offers reassurance that your loved ones will remain financially secure no matter what happens. This give you a much needed assurance to live and work overseas with confidence and peace of mind.

Life insurance needs evolve with age and career growth. Here is how buying the right policy at different life stages can help young professionals build financial security and long-term stability:

Age Group Life Insurance Benefits Early 20’s, Start Early and Build Security When you begin life insurance at a young age, you are guaranteed the lowest premium rates and long-term coverage benefits.

It assists in establishing a good financial foundation and developing disciplined saving habits before major responsibilities arise.Whole Life Insurance Provides cover throughout one’s lifetime with a guaranteed death benefit, supporting long-term financial security. Also helps create a financial legacy for heirs. 20 to 30 years, Secure Your Future Goals This is the ideal time to protect increasing income and future aspirations. Life insurance helps manage debt, save for a house, and begin long-term wealth building. 30 to 40 years, Protect Your Family and Their Dreams With growing family and career responsibilities, life insurance ensures your dependents remain financially secure and supports goals like children’s education and retirement planning. 40 to 50 years, Prepare for Retirement This phase focuses on strengthening financial stability. Savings or annuity-based life insurance helps stabilise risk, preserve wealth, and build post-retirement income. 50 years and above, Leave a Legacy Life insurance at this stage helps maintain your family’s financial independence, covers final expenses, and supports estate planning and legacy creation. Life insurance policies come with specific exclusions where the insurer will not pay the death benefit. Understanding these exclusions is important to avoid claim rejections and be fully aware of the policy’s limitations.

- 1. Death Due to Suicide Within the Waiting Period

Most life insurance policies include a suicide clause, especially within the initial policy period, typically the first two years. If the person who is covered under the insurance policy dies by suicide during this time, the insurer may deny the claim or only refund the premiums paid.

This clause exists to prevent misuse of insurance for financial benefits. After the waiting period passes, many policies cover cases like these under certain conditions. The exact terms vary between insurers and must be carefully reviewed before purchase.

- 2. Death caused by involvement in criminal activities

Deaths resulting from participation in illegal or criminal activities are generally not covered by life insurance policies. If a policyholder dies while committing a crime or engaging in unlawful acts, the insurer has the right to reject the claim. This includes violent crimes, fraud etc. These exclusion are there to ensure insurance is not used to benefit from risky or unlawful behavior.

- 3. Death due to drug abuse or intoxication

If a policyholder’s death occurs due to excessive alcohol intake or drug abuse, the claim may be denied. Insurers often include this exclusion to limit liability where risky behavior directly contributes to demise. This can include accidents or diseases caused by intoxication or overdose.

Some policies give you some freedom in this area depending on the circumstances, but in most cases, substance abuse-related deaths are excluded. It is important for insured people to understand how their lifestyle can lead to coverage related limitations.

- 4. Death during hazardous activities

Life insurance policies usually exclude deaths that occur while engaging in high-risk activities, such as adventure activities, skydiving, or deep-sea diving. These activities put you at higher risk for saccidental death, and unless specifically covered through an add-on or rider, claims may be rejected.

Individuals who participate in such activities should disclose this information when purchasing a policy. Some insurance companies offer customized coverage options, but failure to declare such risks can cause complications during claim settlement.

A life insurance policy is a contract between you and an insurance company. You pay regular premiums, and in return, your family gets a financial payout if something happens to you. This life cover pay out can help with daily expenses, paying off loans, and future financial needs like children’s education.

Choosing the best life insurance as per your needs ensures financial security for your loved ones. Policies differ in coverage, policy tenure, and premium costs, so comparing options helps find the best fit. While all life insurance policies provide life cover benefit, some plans also offer additional benefits such as savings/investment benefits along with tax benefits. The right life insurance policy gives your family stability and peace of mind.An insurance policy is basically a legal contract between your insurance company, i.e. insurer and the person being insured. It clearly defines the sort of claims the insurer is concurring to pay along with the various obligations set for both insurer and the insured.

The life insurance coverage amount, also known as the death benefit, is the amount of money that the insurance company will pay to the beneficiaries of the policy in the event of the policyholder's death. This amount is typically determined at the time the insurance policy is purchased and can be adjusted as needed.

When choosing a coverage amount, it's important to consider several factors, such as:- Current and Future Income: If you have dependents who rely on your income, you should consider how much money they will need to cover living expenses and maintain their standard of living in the event of your death.

- Debts and Loans: If you have outstanding debts or a loan, you should consider the amount of money needed to pay these off in full.

- Future Financial Goals: If you have future financial goals, such as saving for a child's education or retiring comfortably, you should consider the amount of money that will be needed to achieve these goals.

- Final Expenses: The cost of funeral and burial expenses, as well as any outstanding debts or bills, should be considered when determining the coverage amount.

- Other Coverage: If you have other forms of insurance policy, such as a disability policy or an employer-sponsored life insurance policy, you should consider how these policies may affect the amount of coverage you need.

It's important to regularly review your life insurance coverage amount to ensure that it still meets your needs and protects your loved ones adequately. An insurance agent or financial advisor can help you determine the right coverage amount for your needs.

Insurance claims are subject to rejection in many circumstances, irrespective of their types. Even if you have the best life insurance plan, we recommend you follow these steps in order to avoid rejection of your life insurance policy claim:

- Disclose Accurate Details: When purchasing life insurance policy (or any insurance), make sure the information you provide/declare in your policy documents, especially lifestyle habits and any existing medical conditions, is correct.

- File Claims Promptly: File your claim with your insurance company at the earliest possible time following an incident.

- Keep Nominee Info Updated: Do mention the name of your beneficiary in all your active policies. At the same time, make sure you inform them all about your active policies.

- Pay Premiums Regularly: Always make your premium payment on time to ensure that the policy remains active and avoids lapsing.

- Fill Forms Carefully: Duly fill the claim form on your own, and try to avoid any mistakes or typos in the form.

When it comes to claims, it is recommended to choose the best life insurance company with the highest claim settlement ratio (CSR). The higher the CSR, the higher the chances of your claim acceptance, provided you produce all required documents.

It refers to the amount payable to a nominee after the event of the unfortunate demise of the insured, as specified in the chosen life insurance policy. You can use an online life insurance premium calculator to get an estimate of the best life insurance premium payable for a specific sum assured.Annualised Premium is essentially the amount specified in the insurance policy schedule, and denoted as the Premium payable during a Policy Year chosen by you (as policyholder), excluding any additional premium paid for the Underwriting, loadings for modal premium, Rider Premiums and applicable taxes, cess, or levies, if any;It is the duration for which the insured is covered under a life insurance policy. It can be different from the premium payment term/period during which you need to pay a life insurance premium.

Badhta Bharosa with 99.8%

Death Claims Paid Ratio^

Useful Resources for Customers

NPS Calculator

Check your estimated retirement corpus with our free nps calculator.

Income Tax Calculator

Easily calculate your income tax liability with our online tax calculation tool.

Pension Calculator

How much do you need for a comfortable retirement? Check with our pension calculator.

BMI Calculator

Check how much extra kilos you want to shed or gain with our BMI Calculator today.

SIP Calculator

Our SIP calculator helps you to determine ideal SIP amount for your financial goals.

NSC Calculator

Quickly check maturity value and interest amount with free online NSC calculator.

Income Tax Slab 2025-26

Stay up-to-date with latest Income Tax Updates

Term Insurance Tax Benefits

Learn how to save tax with your term plan

Types of Life Insurance?

Explaining different Insurance Categories

What is Investment?

Know more about Savings Options

What is Term Insurance?

Understand how Term Plans work.

What is ULIP?

Insurance products offering savings and life cover

Customer Testimonials

Real Folks with Real Stories!

See what our customers feel about Axis Max Life Insurance products and services. Our esteemed customers like you help us to provide better solutions.

Usha Kumar

Akanksha Goyal

Sreedharanunni. S

Jagriti Mishra

Axis Max Life's Best selling Insurance Policy

- 5 Plan variants to cater to different life stage needs

- Enhance protection through rider integration.

- Systematic money withdrawals as per your desire from your policy.

- Unlimited Free Fund Switches & premium redirection

- USD denominated global investment from GIFT City.

- Choice of global equity, debt & commodity funds.

- Unlimited free fund switches & premium redirections

- Survival Benefit payable over the policy term subject to 4 plan variants

- Flexibility of choice of both policy term and premium payment term.

- 'Save the date' feature - Choice of date in a year to receive survival benefit

- 3 variants that help you plan and achieve future milestones

- Choice of death benefit to be in multiples of 5 or 7 to 11 times the annualise premium paid.

- Boost income via Flexi income option available in the first policy year

- Survival Benefit payable over the policy term subject to 4 plan variants

- Flexibility of choice of both policy term and premium payment term.

- 'Save the date' feature - Choice of date in a year to receive survival benefit

- ULIP charges, deducted under the policy, added back to fund value, subject to the plan variant chosen

- Guaranteed Loyalty Additions provided from the end of 8th policy year onwards depending on premium band chosen.

- Multiple fund options and investment strategy based on your risk profile

- Get level sum assured throughout the Policy Term

- Empower the nominee to choose the payout mode, at claims stage

- Additional coverage against the risk of Accidental death

- Level sum assured throughout the Policy Term

- Empower nominee to choose the payout mode, at claims stage

- Additional coverage against the risk of Accidental death

- Option to take your premiums back subject to T&Cs.

- Premium break option twice during policy term to avoid paying policy premium

- Exit the policy with a one-time special exit value option for base cover only.

- Joint Life Annuity, where your partner continues to receive the annuity in your absence.

- The nominee will receive the total premium as the lump sum death benefit upon the annuitant's death.

- Flexible annuity pay-out: monthly, quarterly, half-yearly, or yearly.

- Inflation-friendly income post retirement with growing annuity

- A wide range of annuity options to fund your life agyer retirement.

- Flexible premium payment and personalised income timings

- Guaranteed income for lifetime

- With Deferred Annuity variant, the nominee gets a minimum of 105% of the purchase price of the policy after the death of the annuitant(s).

- Joint Life Annuity - your partner continues to receive annuity in your absence.

- On the Vesting Date, a benefit equal to the Fund Value will be paid to the you.

- Higher of fund value or 105% of total premium payable to the nomineed in case of death of the insured during premium payment phase

- Unlimited & Free Fund Switches

- Choice of Immediate and Deferred Annuity options

- Choice of guaranteed proportion under Variable Annuity

- Choice of guaranteed proportion under Variable Annuity

* As per financials closed on 30th June 2026

Awards

Your Life Insurance Policy with easeConvenience at Your Fingertips with Axis Max Life Insurance Mobile App

Download

Companies who’ve trusted Axis Max Life Insurance

As a member of a rapidly evolving Industry, Axis Max Life Insurance is one of the trusted name amongst the several most admired companies in financial domain. Let’s quickly have a look at some of these companies who entrusted our vision.

Contact Us

if you got any question for us?Connect on WhatsApp

+91-7428396005Customer Care

1860-120-5577For On-going Applications/Buying a New Plan

+91-124-648-8900FREQUENTLY ASKED QUESTIONS

Why Should You Have Life Insurance?

Can I Choose the Policy Term and Premium Payment Term When Buying Life Insurance?

What Are Life Insurance Quotes?

Who Needs Life Insurance the Most?

What are the Types of Life Insurance Plans?

Life insurance is not a single product; instead, it has many forms. Most common types of life insurance include term plans, unit linked insurance plans, endowment plans, and retirement plans.

Thus, you need first to understand the working of each form of life insurance and then compare between plans to see which one suits you the best.

What Are the Key Factors That Affect Life Insurance Premiums?

What Are the Uses of Life Insurance?

Do I get survival benefits under my life insurance policy?

What will happen if the life insurance premium is not paid on time?

Who decides the life insurance premium?

What is a life insurance premium?

How to choose the right sum assured under life insurance?

Why buying life insurance is important?

What are life insurance riders?

They allow you to tailor your plan for additional protection at a small extra cost.

Why add riders to your term life insurance policy?

Thus guaranteeing higher levels of financial security without the need for an additional policy.

What is a premium in insurance?

What is underwriting in life insurance?

It involves reviewing your age, health, lifestyle, occupation, and medical history to determine your eligibility and premium amount.

How is an insurance premium calculated?

The less risky your profile is, the lower your premium will be.

Is the insurance premium monthly or yearly?

Many people prefer annual payments to avoid frequent reminders and missed due dates.

Why is life insurance a safe investment?

What are the types of death not covered in life insurance?

The following are some of the circumstances under which a life insurance company can turn down a death claim:

- Murder of the policyholder and the nominee is involved

- Death due to criminal involvement

- Death under the influence of alcohol or drugs

- Non-disclosure of smoking habits

- Death during hazardous or adventure activities

- Death through pre-existing illnesses

- Death during childbirth or pregnancy complications

- Suicide during the first year of the policy

- Death as a result of a natural disaster

Always check for latest inclusions/exclusions by regulator to stay up to date

Can I withdraw money from my insurance policy?

Yes, you can withdraw money from your insurance policy, but it will depend on the kind of life insurance plan you have:

- In term insurance, there is no withdrawal or cash value privilege available.

- In endowment, money-back, or ULIP policies, you can withdraw part of the funds after a certain lock-in period or receive a surrender value if you decide to end the policy early.

What is a mutual fund?

How risky is it to invest in mutual funds?

Should I invest in a money back plan?

What is an endowment plan, and should I buy it?

What are some tax-saving investment options for me

What are the 3 benefits of term insurance?

The three essential benefits of term insurance include the following:

- Keeping Loved ones financially secure: Term insurance will keep your family financially covered in the event of a premature death of policyholder.

- Plan for Financial Milestones: It enables you to budget significant milestones such as the education of your children or other financial obligations.

- Income Replacement: A term plan is a reliable source of income in difficult periods like critical illness, accidents or after retirement.

Is accidental death covered in term insurance?

What happens at the end of a term life insurance policy?

Nevertheless, when you still require protection, you have the option of renewing your policy to a new term or converting it to a whole life insurance, given the current policy has a conversion option.