Individual

Individual

Health insurance is meant to p ... rovide financial cover against hospitalization costs, prescription fees, medical bills, etc. With soaring medical bills and hospitalization costs, buying health insurance has become more than just an option; it has become a necessity if you seek the best medical care without worrying about the financial strain it might bring on your wallet. One can get health insurance against regular premium payments. These premiums depend on age, medical conditions, coverage, policy term, etc. Ensure that you find the best health insurance plans and additional riders that meet all your future medical requirements. Read More

Health Insurance Plans

64 Critical

Illnesses Covered@>

Tax Savings

upto ₹54,600~#

3 Hours

Claims Promise^*

99.8%

Death Claims Paid Ratio^

Health Insurance Plans

₹10 lakh cover @₹542/Month for 64 Critical Illnesses@>

Health insurance is meant to p ... Read More

- 64 CriticalIllnesses Covered@>

- Tax Savingsupto ₹54,600~#

- 3 HoursClaims Promise^*

- 99.8%Death Claims Paid Ratio^

Reviewed by Vaibhav Kumar

Last Modified 9th July 2026 Insurance Domain Expert With over 16 years in life insurance, Vaibhav Kumar is a recognized products and digital leader for driving innovation at Axis Max Life Insurance. He's played a pivotal role in developing new business lines and implementing successful D2C strategies.

Health insurance plans in India are basic indemnity-based insurance products, which are specifically designed to provide financial assistance against medical expenses incurred in case of hospitalization or critical illnesses.

- Health insurance in India is a contract between an insurance provider and a customer which promises the insurer to pay for the medical bills if the policyholder is injured or sick in the future, resulting in hospitalization.

- Health insurance covers medical expenses, which includes hospitalization & treatment charges along with surgeries or any other medical cost.

- Generally, insurance companies who provide the best health insurance plan in India are associated with a vast network of hospitals, which ensures convenient cashless treatment for the policyholders.

- Furthermore, a health insurance policy also helps you cope with the work-pay loss while undergoing treatment, which may otherwise cause imbalances in your family finances. In other words, having coverage with the best health insurance in India will enable you to opt quality medical treatment without burdening your savings.

Health insurance plan works as a financial protection tool that help you during medical emergencies. For this, you have to pay a regular health insurance premium as per the agreed terms and conditions. You will get coverage of your medical bills up to the limit you have selected. A simple real-life case will make it easier for you to understand.

Mohit, a healthy 25-year-old from Bangalore, decides to opt for a health insurance for ₹10 lakhs to protect himself against future medical costs. He pays a monthly premium of ₹409 for this. In the third year, Mohit, got infected with severe malaria followed by a hospitalisation for a week.

The total hospital charges sum up to ₹3 lakhs. As he was hospitalised at a network hospital under a cashless facility, the insurance company paid the ₹3 lakh bill directly. Before renewing the policy, Mohit can avail the benefits of the remaining sum insured of ₹7 lakhs.

Therefore, health insurance, in a way, offers a financial safety net during medical emergencies. It helps you cope with unplanned healthcare costs without exhausting your savings.

Family's Financial Planning Starts Here

- High life cover at affordable premiums

- Death Claims Paid Ratio 99.70%^

- Coverage against 64 critical illnesses@

Since one size does not fit all, there are also different types of health insurance plans available in the market. Several factors such as your age, family size, and medical history play a vital role in the plan selection. Let’s see quickly what are the different types of health insurance plans in India meeting various medical and related financial needs:

- Individual Health Insurance: This type of policy covers only one person under the insurance plan. The entire sum insured is available to that individual, ensuring full financial protection. This is one of the best individual health insurance plan options available and perfect for individuals without dependents.

- Family Floater Health Insurance: It is a single policy covering more than one family member. All members who share the sum insured can use the plan's benefits whenever needed. It is a cost-effective and appropriate choice for couples, people with children, and dependent parents.

- Critical Illness Insurance: This type of policy offers a lump sum if you are diagnosed with any of the listed serious illnesses. With this you get help in managing costs of treatment, including any loss of income, since it covers diseases like cancer, heart attack, stroke, or kidney failure as per the policy.

- Cancer Insurance Plan: The plan is designed to cover the cancer’s different stages. Upon diagnosis, it may provide staged pay-outs. It even offers salary benefits during treatment. The received monetary aid can be used to pay medical bills and keep the household running.

- Senior Citizen Health Insurance: An insurance product made for the senior citizens, who are 60 years old or above. It not only covers age-related diseases but also the high medical risks that are typically expected in later years. Undoubtedly, it works as a financial shield against rising healthcare costs.

- Maternity Health Insurance: This type of insurance covers pregnancy-associated costs, including delivery and newborn care. It comes handy for managing hospital bills after having a baby. However, there is a waiting period before making claims for some or all of the pregnancy-related hospital charges.

- Top-Up and Super Top-Up Plans: Under this offer, you get extra coverage if the sum insured of the base policy is exhausted. This is an extremely cost-effective way to increase health insurance coverage at relatively low premiums.

- Group Health Insurance: Employers offer this product to employees as part of their workplace benefits. Usually, the employer pays the premium in full or in part. So, the employees covered receive affordable health coverage and financial protection against medical expenses during their employment.

The most appropriate health insurance plan is the one that suits your circumstances, including your stage of life, family responsibilities, and financial goals.

Health insurance plans provide comprehensive coverage against the medical costs associated with the treatment of life-threatening ailments such as cancer and other medical emergencies. With comprehensive health insurance coverage, you can protect your finances while your medical insurance plan takes care of the high medical bills, hospitalization, and other treatment expenses. Here are a few benefits of investing in the best health insurance policy in India

1. Comprehensive Coverage Against Medical Treatment Expenses

Having health insurance enables you to receive the best possible care in case of a medical emergency, without putting any strain on your savings. In other words, the best health insurance company in India will offer comprehensive protection against medical costs, which may increase rapidly depending upon the situation.

2. Additional Financial Protection Against Critical Illnesses

Some health insurance companies in India offer critical illness insurance protection, either as a rider add-on or as a standalone health insurance policy. Having health insurance coverage, together with critical illness cover, provides financial protection against several life-threatening ailments such as kidney failures, cardiovascular issues, bone marrow transplants, stroke, and accidental dismemberment. Common critical illnesses covered under Axis Max Critical Illness & Disability Rider include:

- Cancer of Specified Severity (malignant tumor)

- Angioplasty

- First Heart Attack – of Specified Severity

- Open Heart Replacement or Repair of Heart Valves

- Surgery to Aorta

- Cardiomyopathy

- Primary Pulmonary Hypertension

- Open Chest CABG

- Blindness

- Chronic Liver disease

In case you are diagnosed with a critical illness included under the predetermined list of your health insurance policy, you are eligible to receive a significant amount as a lump sum. You can utilize this amount to meet your daily expenses, illness-related treatment costs, and any other requirements.

3. Avail of Cashless Treatment Across Leading Network Hospitals

The health insurance plans in India, also offer cashless claim facilities across any of the leading hospitals in the country. In cashless treatment, the treatment costs are borne by your health insurance provider as they directly settle the hospitalization expenses with on your behalf.

To avail of cashless treatment benefits, however, you have to seek admittance at any of the network hospitals as prescribed under your health insurance policy. Furthermore, you may have to fill out a pre-authorization form and provide your health insurance card to avail of the cashless treatment facility

4. Significant Tax Saving Benefits4

To promote awareness and access to comprehensive health insurance plans to the masses, the government offers significant tax-deductions on the premium paid towards the health insurance policy.

Axis Max Life Secure Earnings & Wellness Advantage (SEWA) Plan offers similar tax benefits on investment along with health insurance cover and investment benefits.

Accordingly, the premium paid towards your health insurance policy is eligible for tax deduction under Section 80D as per income tax act 1961 (under old tax regime). The quantum of tax deductions under your medical insurance plan is as below:

- a) If you purchase health insurance coverage for your spouse, children and yourself, you can save up to Rs 25,000 as tax deductions.

- b) By including your parents (below 60 years of age) under your health insurance coverage, you can avail of additional tax deductions up to Rs. 25,000, to take your total tax savings up to Rs. 50,000

- c) In case your parents are ageing 60 years or above, the total amount of tax savings may increase up to Rs. 75,000

- d) You can also avail of a deduction of Rs. 5000 towards payment of preventive health check-up of your spouse, dependent children, parents and yourself

| Covered Individuals | Exemption Limit | Health Check up Exemption Limit | Total Deduction under Section 80D |

|---|---|---|---|

| Self, spouse and dependent children | Rs 25,000 | Rs.5,000 | Rs. 25,000 |

| For self and family including parents (all under 60 years of age) | Rs. 25,000 + Rs. 25,000 | Rs.5,000 | Rs. 50,000 |

| For self, family including senior citizen parents | Rs. 25,000 + Rs. 50,000 | Rs. 50,00 | Rs. 75,000 |

| For self and family members including parents (all above 60 years of age) | Rs 50,000 + Rs. 50,000 | Rs. 50,000 | Rs. 1 Lakh |

*Note: The maximum deduction for preventive health check-ups, of up to Rs 5,000 shall be allowed for payment made towards such health check-up of your spouse, dependent children, parents and self, under Section 80D

4Tax benefits as per prevailing tax laws, subject to change

Health insurance add-ons are basically additional coverage options that you can link to your primary health insurance policy to get better protection. They function like upgrades. Your primary plan covers the basics, and add-ons let you extend it to suit your needs. These choices can make your policy more functional and personalised.

There are various types of add-ons that you can choose from:

OPD Cover

It covers expenses for doctor consultations, diagnostic tests, and medicines that do not require hospital admission. These are typical medical costs that many families incur frequently.

It helps cover minor healthcare expenses and is a good fit for families with kids, elderly parents, or anyone who frequently sees a doctor.

It helps cover minor healthcare expenses and is a good fit for families with kids, elderly parents, or anyone who frequently sees a doctor.

Critical Illness Cover

This type of insurance provides a payout when a person is diagnosed with a serious illness, such as cancer, stroke, or heart disease. The amount can be used for both treatment purposes and meeting other financial requirements.

It takes care of your financial needs during a major health crisis. This also serves as a great help to individuals with a family history of serious diseases or those wanting an extra layer of protection.

It takes care of your financial needs during a major health crisis. This also serves as a great help to individuals with a family history of serious diseases or those wanting an extra layer of protection.

Maternity Coverage

This covers expenses related to pregnancy, delivery, hospital, doctor’s fees, and care for the newborn. Giving birth in a private hospital can be extremely expensive.

This add-on reduces the financial burden during pregnancy and delivery. So, it is a good choice for those planning for parenthood.

This add-on reduces the financial burden during pregnancy and delivery. So, it is a good choice for those planning for parenthood.

Day-Care Treatment Cover

Covers medical treatments that require hospitalisation for a very short period, such as dialysis and minor medical operations.

You will be able to focus on your recovery, as the insurance company will cover the medical bills for your short-term admission. It can be a good support system to keep medical expenses controlled for elderly people or patients with chronic medical conditions.

You will be able to focus on your recovery, as the insurance company will cover the medical bills for your short-term admission. It can be a good support system to keep medical expenses controlled for elderly people or patients with chronic medical conditions.

Room Rent Waiver

This option allows you to choose any hospital room category without any restrictions. You can opt for a better room without worrying about additional charges.

Aside from saving you from paying extra at the hospital, it is also a nice option for families who want to choose the kind of comfort during a hospital stay.

Aside from saving you from paying extra at the hospital, it is also a nice option for families who want to choose the kind of comfort during a hospital stay.

Personal Accident Cover

In case of accidental death or permanent disability, this insurance provides financial support to the insured or their family.

It is a good way to ensure that, even if you are unable to work due to an accident, your family receives financial support. This is primarily designed for the family's primary earner.

It is a good way to ensure that, even if you are unable to work due to an accident, your family receives financial support. This is primarily designed for the family's primary earner.

Home Healthcare Cover

This means you will get cover for medical care at home under professional medical supervision, for example, nursing care and physiotherapy.

With this, you will need fewer hospital visits. Elderly people or patients who need long-term care will benefit the most from such a cover

With this, you will need fewer hospital visits. Elderly people or patients who need long-term care will benefit the most from such a cover

Your lifestyle, health, and family commitments will determine which add-on you need. Besides consolidating your health insurance, these options also give you a wider financial safety net.

India’s healthcare landscape is undergoing change. While medical infrastructure is improving, rising lifestyle diseases, increasing treatment costs, and communicable disease threats continue to make health risks complicated.

Understanding these trends is essential for smarter health planning and financial protection.

Reducing Out-of-Pocket Expenses

OOPE fell to 39.4% of total health spending in 2021-22, down from over 64% almost a decade ago.

With more people opting for insurance and government schemes expanding coverage, Indians are paying slightly less directly from their pockets. However, the remaining burden is still significant, especially during emergencies.

With more people opting for insurance and government schemes expanding coverage, Indians are paying slightly less directly from their pockets. However, the remaining burden is still significant, especially during emergencies.

Increase in Private Insurance Contribution

Between 2013-14 and 2021-22, private health insurance spending roughly doubled (118% increase).

Rising awareness and higher medical bills are pushing families toward private insurance, making it a key pillar of healthcare financing.

Rising awareness and higher medical bills are pushing families toward private insurance, making it a key pillar of healthcare financing.

Rising Healthcare Costs

Healthcare costs in India are projected to grow by 13% in 2025, per a recent medical trend report.

Inflation in medical services, advanced treatments, and costly diagnostics mean even routine healthcare has become more expensive, increasing the need for financial cushioning.

Inflation in medical services, advanced treatments, and costly diagnostics mean even routine healthcare has become more expensive, increasing the need for financial cushioning.

Growing Premiums

According to the Economic Survey, the health insurance sector is growing, premiums grew by 11% in FY 23, and health insurance made up roughly 35% of all non

life insurance premiums.

With more people taking insurance, insurers are expanding coverage—but rising premiums also show increasing medical risks and treatment costs.

With more people taking insurance, insurers are expanding coverage—but rising premiums also show increasing medical risks and treatment costs.

Beyond financial trends, India faces growing medical challenges that make healthcare planning more critical than ever.

1. India’s Load of Chronic Diseases (NCDs)

Noncommunicable diseases like diabetes, heart disease, and hypertension in India have increased from 37.9% in 1990 to 61.8% in 2016. Approximately one in four Indians faces the risk of dying from an NCD before reaching the age of 70. Sedentary lifestyles, pollution, and dietary habits are accelerating these conditions even among younger adults.

2. India’s Cancer Risk

Cancer cases in India are rising sharply, with breast, lung, cervical, and oral cancers leading the list. Early diagnosis is quite low due to awareness, making treatments more complex and expensive.

3. Viral Hepatitis Becoming a Public Health Threat

Hepatitis B and C infections continue to increase despite being preventable. Untreated, they can lead to chronic liver disease, cirrhosis, and liver cancer, adding long-term healthcare costs.

4. Accelerated Cost of Living with Diabetes

India is called the Diabetes Capital of the World, hosting over 100 million diabetics. India has been called “the diabetes capital of the world,” and it is estimated that 41 million Indians have the disease and “every fifth diabetic in the world is an Indian."

The cost of insulin, regular tests, consultations, and complications makes diabetes one of the most expensive long-term conditions to manage.

The cost of insulin, regular tests, consultations, and complications makes diabetes one of the most expensive long-term conditions to manage.

5. India’s Threat of Communicable Diseases

Dengue, malaria, tuberculosis, and seasonal viral infections continue to affect people. Rapid urbanisation and climate change are keeping these diseases active despite medical advancement

6. The Burden of Cardiovascular Diseases

Heart diseases remain the leading cause of death in India. Unhealthy lifestyles, stress, air pollution, and genetic predisposition are causing heart attacks at earlier ages than ever before.

Before we dive deeper, it’s important to first understand what is health insurance . Knowing this basic definition helps you clearly see why health insurance is essential for your life.

Health insurance is a financial product to help you cover medical expenses arising from illnesses, accidents, or hospitalization. A health insurance policy may cover hospital bills, diagnostic tests, surgeries, day-care procedures, and sometimes preventive health check-ups.

Healthcare costs are increasing every year. In fact, last year India witnessed a healthcare cost inflation of 14%, making even basic treatments expensive.

As per a research study by Frontiers in Public Health, almost 50% of healthcare expenses in India are still paid out of pocket, compared to the global average of about 20%. This is a big reason to set aside a small budget for your health insurance premiums.

Rising medical inflation makes every hospital visit a potential financial shock. A good health insurance plan protects you from these sudden expenses by covering hospital bills, diagnostic tests, surgeries, day-care procedures, and sometimes preventive check-ups.

1. Chronic Disease Management

With the rise in lifestyle diseases such as diabetes, thyroid disorders, and heart ailments, managing long-term treatments is becoming heavy on pocket. If you have a health insurance, it helps cover consultations, tests, medicines, and procedures related to chronic illnesses.

2. Rising Medical Costs

Medical inflation in India is on the rise. Last year, it increased by 14%, outpacing general inflation in India. Health insurance protects you from rapidly increasing treatment costs and hospitalization charges.

3. Financial Security

Without health insurance, a single medical emergency can wipe out years of savings. A health plan ensures financial stability and prevents medical debt. Families who aren't prepared spend a fortune on health emergencies and the live life under immense burden.

4. Comprehensive Coverage

Modern health insurance plans cover a wide range of expenses, hospitalization, day-care procedures, ambulance charges, and preventive check-ups. This ensures that you stay protected from all sides when a medical emergency hits.

5. Peace of Mind

You’re at peace when you know that any unexpected medical expenses are taken care of. It allows you to focus on recovery instead of thinking about the medical bills.

6. Cover Against Unforeseen Events (Like Accidents)

Accidents can happen anytime and to anyone. And when that happens, they require immediate hospitalization, surgeries, and long rehabilitation periods. Health insurance gives you that financial support you need during tough times.

7. Cover for Life Events (Like Pregnancy)

Many health plans offer maternity benefits, covering pre-natal care, delivery charges, and post-natal expenses, reducing the financial burden during pregnancy. If you’re a woman or a man who is planning to have kids in the future, this is something you need to keep in mind.

Choosing the right health insurance plan in 2026 is mostly about finding a good balance between financial security and premium costs. A good policy shouldn’t only save your money during health emergencies, but also leave your monthly budget intact. Hence, the insurer's trustworthiness must be your primary concern when selecting.

1. Select the Right Type of Policy

Begin by determining the kind of plan that matches your financial and family conditions:

- Individual health plan: Perfect for a single person who has specific needs.

- Family floater plan: One shared cover for the entire family.

- Senior citizen plan: Designed for people aged 60 and above.

- Top-up or super top-up plan: Increases coverage at a lower incremental premium.

2. Decide the Right Sum Insured

The coverage amount should not be random. A practical approach is to select a sum insured that is up to 3 times of your annual household income. Maternity cover is a primary benefit. However, you should also consider:

- City of residence (metro cities require higher coverage).

- Age of insured members.

- Number of family members.

- Family medical history.

3. Check Important Policy Features

An inclusive policy covering various non-treatment costs should reduce your out-of-pocket expenses. Look for:

- No room rent limits.

- Low or zero co-payment.

- Coverage for consumables.

- Pre- and post-hospitalisation expenses.

4. Evaluate the Insurer’s Financial Strength

Before buying, review the insurer’s performance indicators: :

- Claim Settlement Ratio (CSR) must be above 90%.

- Incurred Claim Ratio (ICR) should be in the range of 60%–80%.

- Good service reputation and stable operations.

5. Consider Value-Added Benefits

Additional features may add value in the long term:

- Restoration of the sum insured.

- Wide hospital network for cashless treatment.

- Nationwide coverage.

- No Claim Bonus (NCB).

- Good Claim Settlement Ratio (CSR)

6. Don’t Make a Choice Based on Low Premium Only

A low premium may hide:

In 2026, the finest health insurance is one that is in line with your financial capability, health condition, and future planning. Additionally, it should have a decent coverage and good claims assistance.

- High deductibles or co-payments.

- Limited hospital network.

In 2026, the finest health insurance is one that is in line with your financial capability, health condition, and future planning. Additionally, it should have a decent coverage and good claims assistance.

Axis Max Life Insurance is a good option if you want both life cover and health protection in one plan. The company has a very high claim settlement ratio of 99.8%, meaning most valid claims are paid successfully.

With Life Insurance, it also offers useful add-ons. This includes critical illness and disability riders, as well as special features, such as terminal illness benefits. Axis Max Life Insurance can also be a good option for protecting health due to

- Health Riders: Add-ons like critical illness, total or permanent disability, etc., offered by the company can be helpful. With these, you will receive additional financial support during medical emergencies.

- Good Record of Paying Claims: The organisation has a 99.8% claim settlement ratio. This is indeed a commendable record of paying claims. Additionally, they also provide the service of a dedicated Claims Relationship Officer who can guide you through the claim process smoothly if needed.

- Complete Insurance Coverage: In case of death, disability, or major illnesses, the plans offered by Axis Max Life Insurance are helpful. There are benefits that can continue even after retirement, providing you with long-term financial security.

- Terminal Illness Advantage: Some plans offer the option to receive the full sum assured early if you are diagnosed with a terminal illness. It will be helpful to your family, as they will receive funds immediately for treatment or other urgent needs.

- Flexible Options to Pay: There are various options available, such as Term with Return of Premium, where you will get back all the premiums paid at the end of the policy term if you make no claims. With certain plans, you can also skip premium payments for a limited period if need be. In simple terms, Axis Max Life Insurance allows you to create a combined “life plus health” protection plan. This means you can customise your coverage to your needs and protect your family from both life risks and major medical expenses in a single structured plan.

In India, there are several ways to purchase health insurance, but before buying keep these things in mind:

-

Research Before You Buy: Before finalizing a policy, it’s essential to research different insurers, coverage benefits, exclusions, claim settlement ratios, and network hospitals.

Reviewing customer feedback, exploring multiple plans, and understanding long-term premium costs can help you make an informed choice and avoid surprises. - Customize Your Plan: Most health insurers in India now offer customizable plans where you can adjust the sum insured, add riders such as critical illness or maternity cover, include family members, or select room rent preferences.

Here are different ways to buy health insurance:

- Online: You can purchase health insurance policies online through the official website of insurance companies, insurance aggregator websites, or through the official government websites like the National Health Insurance Scheme (NHIS).

- Agents: You can also purchase health insurance policies through insurance agents, who can guide you through the process and help you choose the right plan.

- Offline: You can also purchase health insurance policies offline by visiting the office of the insurance company or through the agent.

To enroll in health insurance, you will need to provide certain documents such as ID proof, age proof, and address proof. You may also need to undergo a medical test depending on the plan you choose. Once you have provided all the necessary documents and completed the medical examination (if required), you need to pay the premium, and the insurance company will issue you a policy document.

0% GST Benefit

Check out the Premium

₹10 Lakh

The primary purpose of health insurance plans in India is to provide comprehensive financial coverage to you and your family members. Thus, you need to make sure that you are choosing a health insurance policy with sufficient coverage and cost-effective premiums payable.

Here is how you can purchase online health insurance coverage

- Fill in your details for a life/ health insurance plan/ cancer plan

- Add the amount of critical insurance/ cancer insurance coverage (or sum insured) that you need with your online health insurance

- Use an online health insurance premium calculator to arrive at the premium amount payable based on your age, gender, lifestyle preferences, chosen health insurance coverage (or Sum Insured) and Maximum Coverage Age.

Choose the maximum medical insurance coverage tenure as the chances of contracting a critical illness increases with age.

Do not settle only for a low-premium plan when choosing the best health insurance in India. For example, if you want coverage for home medical visits during emergencies, review how much home care is covered, related medical expenses included, and maximum payout limits before purchasing

1. Waiting Period and Pre-existing conditions

It is the time you have to wait before claiming benefits for pre-existing diseases or certain treatments. Pick the health policies with a shorter waiting period. This way you can get full coverage at the earliest, without any problem of your claim getting delayed.

2. Coverage Amount

A very common mistake people do is opting for lower health insurance coverage to save on premiums. This health inflation is rising very rapidly and in next few years, the amount currently considered sufficient will turn out to be insufficient.

3. Co-Payment (Co-Pay)

This refers to how much of the hospital bill you will have to pay yourself, while the insurer pays the remainder. Do not forget to go through the co-pay clause thoroughly. With a low or zero co-payment plan, you can save on out-of-pocket expenses without compromising financial protection.

4. Room Rent Limit

It is the maximum amount your insurer will pay for hospital room charges per day. Go through the room rent caps carefully. Selecting a plan with a higher or no room rent limit will help you avoid additional expenses during hospitalisation.

5. Network Hospitals

These are the hospitals where you can get cashless treatment under your policy. Review the insurer’s hospital network list in your city. A larger cashless network ensures faster admission, smoother claims, and minimal upfront payment during emergencies.

6. Pre- and Post-Hospitalisation

The medical expenditure that you incur before and after hospital admission and discharge, like diagnostic tests, medicines, and follow-ups, is included in the plan. Always verify the number of days your insurance covers. Longer coverage provides more comprehensive financial protection and reduces personal expenses.

7. Day-Care Treatments

These medical procedures do not require 24-hour hospital admission for a patient. Go through the list and check how many day-care procedures are covered in your insurance. Opt for a plan that gives good coverage. It will be pocket-friendly and beneficial.

8. No-Claim Bonus (NCB)

This increases your sum insured each year you go claim-free, without raising your premium. Review the NCB percentage and maximum limit for the plan you select. A higher NCB benefit enhances long-term coverage and improves overall value for money

9. Sub-Limits

These are caps placed on specific treatments, room types, or medical expenses within your overall sum insured. Choose policies with fewer or no sub-limits. This ensures broader coverage, lower costs, and better claim support during hospitalisation.

10. Maternity Benefits

With this policy, you will get coverage for newborn care and pregnancy-related expenses. Find out the waiting period, the maximum coverage, and the terms for inclusion of the newborn. Choose a plan that offers comprehensive maternity coverage to ensure a sound financial plan for childbirth expenses.

11.OPD Cover

It covers the costs of the doctor’s visits, laboratory tests, and small procedures that do not require hospitalisation. Review the OPD limits and inclusions when choosing a plan. OPD benefits can reduce regular medical expenses and improve overall cost savings.

It’s extremely important to understand what your health insurance policy covers, and what it doesn’t. Knowing these details helps you compare your options wisely and increase your health insurance benefits.

What is Covered in a Health Insurance Plan?

Most health insurance plans offer comprehensive protection against medical expenses. Here’s what is typically included:

- Hospitalization Cost: Covers room rent, ICU charges, nursing, treatment costs, and doctor fees during hospitalization due to illness or injury.

- Pre- and Post-Hospitalization: Policies reimburse medical costs for tests, consultations, and medicines before and after hospitalization.

- Day-Care Procedures: Treatments that do not require 24-hour hospitalization, like cataract surgery, dialysis, or chemotherapy, are covered.

- Emergency Ambulance Cover: Financial support for ambulance services used during medical emergencies.

- Cashless Treatment: Avail treatment at network hospitals without paying upfront.

- AYUSH Coverage: Some insurers include Ayurveda, Yoga, Naturopathy, Unani, Siddha, and Homeopathy treatments under their policy.

- Restoration of Sum Insured: Automatically reinstates the sum insured when it gets exhausted during the policy year.

India’s health insurance pricing, particularly medical plan costs, is accelerating faster than the global average. The premiums and underlying healthcare costs are rising year after year. Employers and insurers face continued pressure to budget for higher pay-outs, which impacts both coverage affordability and sustainability.

Cost & Coverage Impact - Health Insurance in India

| Category | Key Points |

|---|---|

| Projected Cost Increase | Medical plan prices in India are forecasted to increase by 11.5 % in 2026. |

| Comparison with Global Trend | Rise in India’s medical cost is significantly above the global average of 9.8 %. |

| Drivers of Cost | Critical medical conditions such as cardiovascular issues and cancer and increased healthcare utilisation are the main factors to cause the cost increase. |

| Impact on Insurance Premiums | Increasing medical expenses result in higher insurance premiums as insurers adjust to claim patterns. |

| Employer Strategy | Companies are responding by allowing flexible benefit plans so as to control the rising health benefit costs. |

| Coverage Implication | Higher costs can reduce affordability of comprehensive coverage for individuals and employers alike. |

This table highlights how rising healthcare costs in India affect both the price of health insurance and the value of coverage under individual plans and employer’s insurance.

Every health insurance policy includes exclusions to prevent misuse and control risk. Common exclusions include:

- Initial Waiting Period: No claims allowed (except accidents) during the first 30 days of policy activation.

- Pre-Existing Diseases During Waiting Period: PEDs are covered only after completing the insurer-defined waiting period, usually 1 to 4 years.

- Cosmetic or Aesthetic Procedures: Cosmetic surgery, plastic surgery, or beautification treatments are excluded unless medically necessary due to an accident.

- Non-Prescription and Lifestyle Expenses: Health tonics, supplements, vitamins, and non-prescribed health items are not covered under typical health insurance plans.

- Dental & Vision (Non-Medical): Routine dental, vision, or hearing care is excluded unless caused by an accident.

- Self-Inflicted Injuries & Substance Abuse: Injuries due to suicide attempts or issues arising from drug or alcohol abuse.

- Unproven or Experimental Treatments: Treatments without sufficient clinical evidence or approval are excluded from most policies.

Self-Employed and Entrepreneurs: If you run your own business or work as a consultant, securing your health is more important. Without an employer-backed cover, you bear the full financial risk of medical emergencies.

Senior Citizens: As age increases, so does the likelihood of medical complications and frequent hospital visits. Senior citizens benefit from specialized senior citizens health plans designed with higher coverage for age-related illnesses, daycare procedures, and OPD treatments.

Individuals Planning for Parenthood: Couples planning to start a family should consider purchasing health insurance early to avail maternity benefits, newborn cover, and related medical support.

People often view buying health insurance as a "future task," but reality is opposite. It should be treate as an essential element to ensure a secure life ahead. Not only for senior citizens and individuals with pre-existing medical conditions, but it is also a prudent decision for individuals across various age groups.

Who should be the first to purchase a health insurance policy?

1. Parents and Families

Being the primary earning member, a medical emergency can completely wipe out the savings. This savings is crucial since you’ve earned it with difficulty. A health insurance policy works as shield help for your savings during a medical emergency. A wide range of coverage will ensure your family receives quality healthcare without having to sell investments or deplete your emergency fund.

2. Individuals with a Family History of Illness

Generally, health plans cover pre-existing diseases only after a certain waiting period. In case your family has lifestyle conditions like diabetes, heart problems, hypertension, etc., then buy insurance early. This way, you can secure your financial well-being without paying huge premiums later.

3. Non-Resident Indians (NRIs)

NRIs often face challenges in finding reliable healthcare coverage in India. Buying a policy online allows NRIs to choose from multiple insurers, compare benefits, and select the best health insurance plan in India. This meets their requirements without physically visiting offices.

4. People with Corporate Cover but Without Individual Cover

While corporate health policies provide basic coverage, they may not meet individual or family-specific needs. Buying an online policy ensures additional protection, higher sum insured, and flexibility to choose the benefits most relevant to you.

5. Independent Women Willing to Secure Your Health

Great news for independent women who are willing to secure their health. Buying health insurance online has become a very easy. Medical emergencies can crop up at any time. So, getting ready in advance is a smart decision to make in current times.

6. People More Than 50 Years of Age

As age increases, medical expenses usually rise. Purchasing health insurance online offers the convenience of comparing senior citizen plans, evaluating pre-existing disease coverage, and selecting policies that provide optimal financial protection and peace of mind.

7. Young Professionals (The Early Birds)

As a beginner, you may feel secure, but this is actually the best time to buy. But why so? When you’re young, the cost of premiums is less because people are usually healthier. Also, an early start can work in your favour as you can get a No-Claim Bonus. This in turn increases your total coverage without a rise in premiums over time during first time hospitalisation.

8. Newly Married Couples

You can switch to a Family Floater Plan to include yourself and your spouse with just one premium. Purchasing the policy early also allows you to complete the maternity waiting period on time. You will be covered when planning a family.

9. Senior Citizens

With old age, health problems become more apparent, requiring frequent doctor visits. Though premiums are higher for these plans, yet they provide the insured with the financial backing needed to cover the costs. This includes costly surgeries, critical illnesses, and hospitalization. Also, it ensures that your retirement funds are safe.

Many Indians still avoid buying a health insurance policy even though medical expenses are increasing every year. This hesitation usually comes from misconceptions and lack of awareness.

1. Dependency on Employer’s Health Insurance Policy

Many people think their employer’s coverage is enough for all medical needs. But the truth is that usually such health insurance plans have low coverage limits.

They may not offer maternity cover or major illness protection. When you switch jobs, you might lose the benefits. This leaves you without protection during critical life stages.

They may not offer maternity cover or major illness protection. When you switch jobs, you might lose the benefits. This leaves you without protection during critical life stages.

2. Unaware of the Benefits of Buying Personal Health Insurance

A major reason for low adoption is low awareness around health insurance. Sometimes people don’t completely understand the benefits that come with a health insurance.

They often assume insurance only helps during hospitalization. The truth is that health insurance plans these days also cover pre-hospitalization tests, advanced treatments etc.

Lack of awareness stops people from choosing better coverage. It also delays buying the best health insurance policy early when premiums are lower.

They often assume insurance only helps during hospitalization. The truth is that health insurance plans these days also cover pre-hospitalization tests, advanced treatments etc.

Lack of awareness stops people from choosing better coverage. It also delays buying the best health insurance policy early when premiums are lower.

3. Unaware of Available Tax Benefits

Many people do not know that health insurance premiums reduce taxable income. You can claim tax deductions of up to INR 1 lakh per year on health insurance premiums under Section 80D (when opting for the old tax regime), which helps further reduce your overall tax burden.

4. Belief That a Higher Sum Insured is Not Required

Some people think a small cover is enough for emergencies, but that underestimates how fast medical costs are rising in India. Serious treatments in private hospitals can easily cross INR 5-10 lakh, forcing you to pay from your own pocket.

In fact, a study in Frontiers in Public Health shows that nearly 50% of healthcare expenses in India are paid out of pocket, not just by people without insurance, but also by those who don’t have adequate insurance cover.

In fact, a study in Frontiers in Public Health shows that nearly 50% of healthcare expenses in India are paid out of pocket, not just by people without insurance, but also by those who don’t have adequate insurance cover.

5. Lack of Awareness About Rising Treatment Costs in India

Many people are not aware of how fast medical costs are rising. Without insurance, treatment delays become common. Awareness of costs often comes only after a medical emergency. Investing early in the best health insurance policy prevents financial distress later.

6. Misconception That Insurance Is Needed Only at Older Ages

A common belief is that health insurance is only for older people. Younger individuals often feel they are healthy enough to not need it. Buying early means you pay lower premiums when you’re younger. It also gives you uninterrupted coverage before lifestyle diseases begin.

Health Insurance Hub

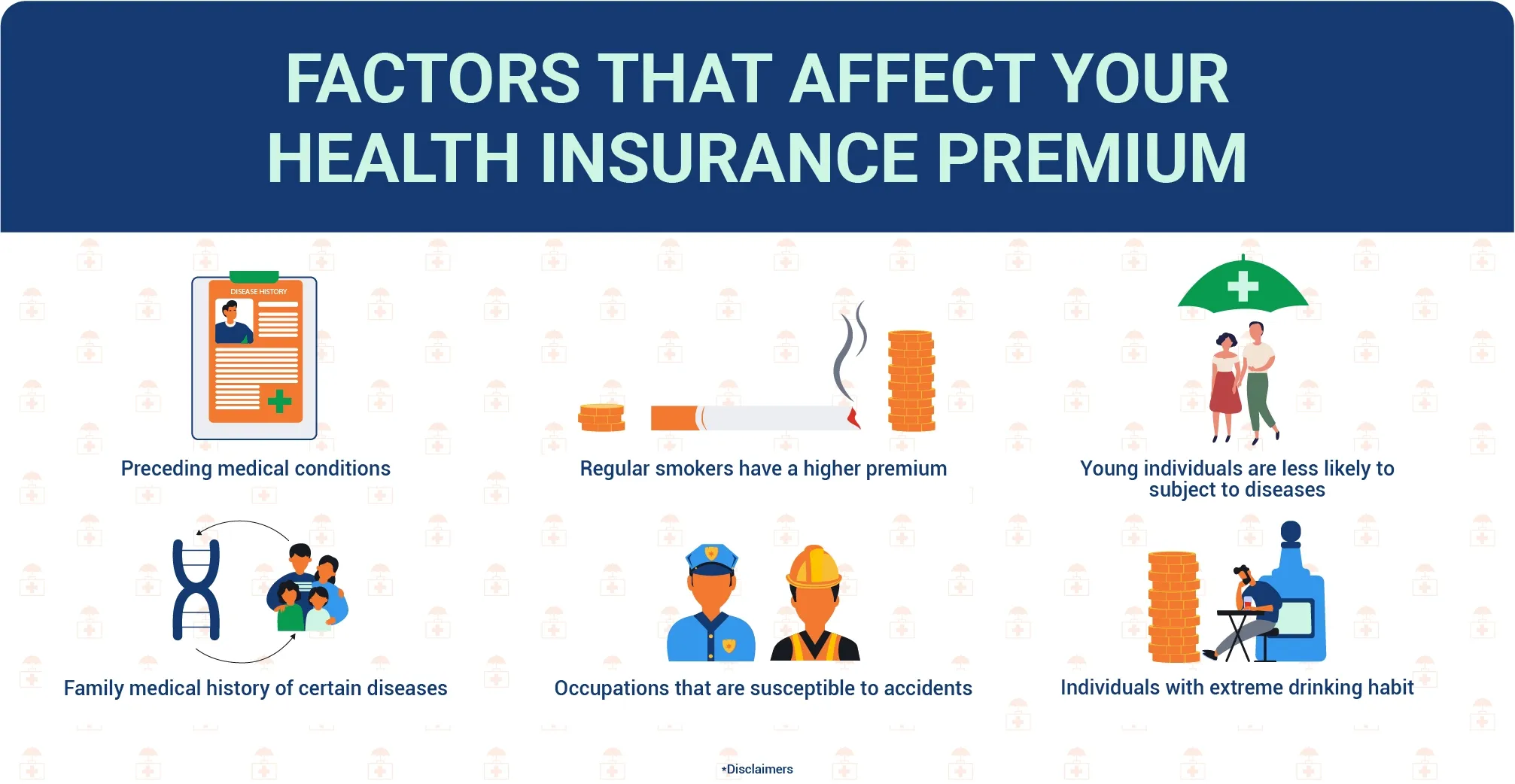

The fast-paced lifestyle that we live today, with so many stressors around us, some unhealthy habits that we adopt might become a roadblock in availing a good health insurance policy. The cost of health insurance plans and the premium amount paid varies significantly for insurers and the insured based on a number of factors:

1. Smoking Status

Your smoking status makes for a huge contributing factor that affects your premium amount as regular smokers are more prone to health diseases and conditions like lung cancer, heart diseases, respiratory disease and more. This vulnerability to a range of ailments affects your health insurance premium amount and you are required to pay a higher price.

2. Alcoholism

Individuals with regular and extreme drinking habits may have to pay higher premiums to get financial security. This is because excessive drinking has been linked to cases of renal and liver disease, high blood pressure, and other serious health issues.

3. Gender Impact

Gender is another factor that can impact premium rates for insurance policies. Typically, women have a longer lifespan than men which makes the premium rates comparatively lower for them.

4. Age

As an individual reaches a certain age, they become susceptible to age-related diseases and medical supervision that adds up to the cost of your health insurance plan.

5. Family Medical History

Some people have a medical history of certain diseases that are passed on to new generations. Such predispositions put some people at a greater risk for diseases. This is also a factor that affects your health insurance premiums.

6. Occupation

Individuals exposed to a stressful or dangerous working environment have higher chances of developing a disease or illness. In case your occupation makes you susceptible to accidents, it can affect your premium rates.

7. Pre-Existing Diseases

Before purchasing a health insurance policy, if you are diagnosed with an ailment, your premium amounts will be higher and requires a set waiting period to avail claims against treatment of such diseases.

Health Insurance policy in India offer coverage which varies from one insurer to another. But, there are few common things which are not covered by some of the best health policy in India. Following are some of the most common health or medical insurance plan exclusions we should be aware of:

- Critical illnesses coverage for pre-existing diseases is subject to a waiting period which can vary from one insurance company to another

- Treatment in abroad or by an under-qualified medical professional

- Pre-existing condition: Defined as a cancer condition (primary or metastatic); pre-cancerous condition or related condition(s) for which the insured had symptoms or was diagnosed earlier or got medical treatment prior to the date on which the policy was issued

- Caused or contributed by (in whole or in part) Sexually Transmitted Diseases AIDS or HIV

- Caused or contributed by (in whole or in part) any of the following:

- Intoxication by alcohol or narcotics or drugs not prescribed by a Registered Medical Practitioner.

- Nuclear, biological or chemical contamination (NBC)

Note: The Health Insurance exclusions mentioned above can vary from one insurer to another. It is recommended to check for all the health insurance inclusion and exclusion before choosing the best health insurance plan in India.

Being familiar with basic health insurance terminology is essential. Beginners may get confused by policy terms, which can lead to claim issues or incorrect decisions. Let’s go through some important terms you should understand:

| Term | Definition |

|---|---|

| Definition | Amount you pay regularly to continue your health insurance. |

| Sum Insured | The maximum amount your insurer will pay for your medical expenses in a year. |

| Deductible | The portion you pay out of your own pocket before your insurance kicks in. |

| Co-Payment | You cover a part of the claim, and your insurer takes care of the rest. |

| Waiting Period | The period you wait until coverage begins for certain conditions or diseases. |

| Pre-Existing Disease (PED) | Any health problem you had before signing up for your insurance plan. |

| Network Hospitals | Hospitals tied to your insurer where you can get cashless treatments. |

| Cashless Claim | A claim type where the insurer pays the hospital directly for treatment. |

| Reimbursement Claim | You pay the hospital bills first, then get the money back from your insurer. |

| No-Claim Bonus (NCB) | If you don’t make any claims in a year, your coverage amounts increase. |

| Sub-Limits | Specific caps your insurer sets on certain treatments or room types. |

| Day-Care Procedures | Short treatments, less than a day in the hospital, still covered by your policy. |

| Exclusions | Health issues, procedures or treatments that your policy does not pay for. |

| Grace Period | Extra time allowed to pay premiums before your policy becomes inactive. |

| Restoration Benefit | Coverage amount is renewed automatically if you use up the full sum insured within the policy period. |

Health insurance eligibility depends on age, medical history, and other factors. Understanding these criteria will help you choose the right plan, ensuring coverage is available when you need it most.

| Eligibility Factor | Details |

|---|---|

| Age Criteria for Adult Policyholders | Adults over 18 can get health insurance. Children’s entry age range starts from from 90 days, depending on the insurer and policy type. |

| Pre-medical Screening | People aged 45 or 55 and above may need a medical check-up before buying health insurance. Generally, senior citizen health insurance requires these tests before coverage begins. |

| Disclosing Pre-existing Diseases (PED) | Any existing illness is covered under the policy only after a waiting period of 1 to 3 years. Insurers will ask about these when you apply. |

Purchasing a health insurance plan at a young age will save you money along the way. You pay less to get better benefits, and you will be ready for any medical needs that may arise later. Generally, young people are healthier and have fewer medical problems. Therefore, insurance companies see them as low-risk customers. Due to this they get policy options at more affordable premium rates. In addition, as healthcare costs continue to rise, early coverage will provide you with financial protection too.

Major Reasons for Buying Health Insurance Early

- Less Premiums: The sooner you buy insurance, especially when you are young, the less you will have to pay in premiums for the same coverage in comparison to those who buy the insurance later on in their lives.

- Fewer Medical Tests: In general, health insurers do not require medical tests for young applicants, so they can get their policies issued more quickly and easily.

- Faster Completion of Waiting Periods: Health plans may have waiting periods for certain conditions. When you purchase a policy at an early stage, you finish these periods while you are still in good health.

- Greater Protection against Future Illnesses: If you develop a health condition later, it may be covered after you have served the waiting period. Buying late may cause the insurer to exclude certain coverages or charge you more.

- No Claim Bonus Benefits: Not making claims for a period of time result in the insurer offering increased coverage or premium discounts. By starting early, you get more time to accumulate this benefit.

- More Plan Options: Generally, younger buyers can choose from a larger number of policies that do not have age restrictions.

In simple terms, buying health insurance early in life will help you retain money, have better coverage, and be prepared, in a healthy way, for future medical expenditure.

In today’s world, medical uncertainties can come at any time. It doesn’t matter what’s your age, lifestyle, or financial status.

This is exactly why a health insurance policy is no longer optional but mandatory. To understand its relevance better, let’s look at some real-life scenarios:

Scenario 1: You’re a young, healthy individual in your late 20s or early 30s with minimal financial responsibilities

At this stage, it’s easy to think that you don’t need a medical cover because you’re fit and active. But, lifestyle diseases and sudden health emergencies can arise anytime. Buying a health insurance policy early ensures:

- Lower premium rates

- Comprehensive coverage for future health risks

- Financial security without disturbing your savings

Starting young also gives you the advantage of choosing from the best health insurance plan in India at an affordable cost, setting a strong foundation for long-term health protection.

Scenario 2: You already have a corporate health cover and don’t wish to spend extra on health insurance

While corporate policies are helpful, they usually come with limited coverage and end the moment you change your job. Depending only on employer-provided health insurance plans can leave you exposed to:

- Inadequate sum insured during critical medical treatments

- Lack of coverage for family members

- Loss of insurance benefits after retirement or job change

A personal health insurance policy ensures uninterrupted protection and acts as a supplementary cover to your corporate plan. .

Scenario 3: You are the sole breadwinner supporting your family

For individuals who solely manage household expenses, education costs, EMIs, and other financial commitments, a medical emergency can result in a big financial loss. The right health insurance plans offer:

- Cashless treatment options

- Protection from high hospitalization costs

- Peace of mind knowing your family is secure

Choosing the best health insurance plan in India can help safeguard both your health and financial future. .

Scenario 4: You have elderly parents or dependents with health concerns

With increasing age come higher medical expenses, frequent check-ups, and a greater likelihood of hospitalization. A comprehensive health insurance policy for senior citizens or dependent parents ensures:

- Coverage for pre-existing diseases

- Access to quality healthcares

- Reduced financial burden during medical emergencies

This scenario highlights why extending coverage beyond just yourself is essential.

Scenario 5: You are a self-employed or gig worker

Freelancers, consultants, and self-employed individuals need to have their own financial safety nets. Having health insurance plans ensure that unexpected medical costs don’t disrupt your income flow.

Scenario 6: You are an independent woman managing your finances and responsibilities

As an independent woman, balancing work, personal responsibilities, and financial planning is part of your everyday life. Unexpected medical expenses can wipe out your savings and long-term goals. A dedicated health insurance policy helps you:

Health insurance empowers you to stay secure and self-reliant no matter what life brings.

- Stay financially independent during medical emergencies

- Access quality treatment without relying on others

- Protect your savings and investments from sudden healthcare costs

Health insurance empowers you to stay secure and self-reliant no matter what life brings.

Scenario 7: You are a housewife taking care of your family

As a homemaker, you may not have a fixed monthly income, yet your health is vital for your family’s wellbeing. A medical emergency without insurance can put tremendous pressure on household finances. With a health insurance plan, you get:

- Coverage for hospitalization and treatment

- Financial support during unexpected illnesses

- Peace of mind for you and your family

Scenario 8: Your family has a history of critical illnesses

As a homemaker, you may not have a fixed monthly income, yet your health is vital for your family’s wellbeing. A medical emergency without insurance can put tremendous pressure on household finances. With a health insurance plan, you get:

This makes health insurance essential for families with hereditary medical concerns.

- Coverage for hospitalization and treatment

- Financial support during unexpected illnesses

- Peace of mind for you and your family

This makes health insurance essential for families with hereditary medical concerns.

Scenario 9: You have young children and want to secure their future

As a parent, your priority is your children’s health and financial security. A medical emergency can drain your savings and affect future plans like education. The right health insurance plan offers:

- Coverage for family floater policies

- Protection from rising child healthcare costs

- An assured safety net for your children

Scenario 10: You’re planning to start a family soon

Pregnancy, childbirth, and newborn care involve medical expenses. Maternity costs are rising every year, and many insurance policies have waiting periods. Getting insured early helps you:

A comprehensive health insurance plan makes your family-planning journey smoother and stress-free.

- Receive maternity and newborn coverage when needed

- Avoid large out-of-pocket medical expenses

- Prepare financially for planned or unexpected complications

A comprehensive health insurance plan makes your family-planning journey smoother and stress-free.

Scenario 11: You live in a metro city with rising healthcare costs

Healthcare in metro cities is significantly more expensive than in smaller towns. A single hospitalization can cost lakhs of rupees. To safeguard yourself from escalating medical bills, a health insurance policy provides:

- Adequate sum insured suitable for metro cities

- Cashless treatment in top hospitals

- Protection against inflation-driven medical costs

- Living in urban areas makes health insurance an absolute necessity.

Scenario 12: You are approaching retirement with limited income sources

As retirement approaches, income often decreases while healthcare needs increase. Relying solely on savings may not be sufficient. A health insurance plan offers:

- Coverage for age-related illnesses

- Reduced financial burden on your family

- Security during medical emergencies when income becomes limited

Following are some of the documents that you might be asked to furnish while buying health insurance plan in India:

- Age Proof

- Identity Proof

- Address Proof

- Medical Reports

- Passport size photo

Note: The list of documents required might vary from one health insurer to another.

With the Indian government introducing 0% GST on health insurance premiums, buying a policy has become more cost-effective for individuals and families.

This change directly reduces your overall premium, allowing you to have quality coverage at a lower price, without feeling the burden of additional taxes.

For example: Earlier, if you purchased a health insurance policy with a premium of INR 20,000, you would have to pay an additional 18% GST, which amounts to INR 3,600.

So, the total cost would have been INR 23,600. With the new 0% GST, you now pay just INR 20,000 for the same coverage, saving INR 3,600 instantly.

Purchasing a health insurance plan online has made our lives easier and what makes it even more convenient is the option to compare various plans online to help you get the best one. Here are some important benefits of comparing health insurance plans online:

- Ease of access to a wide range of health insurance plans

- As per your health requirements, income, and age, you can get free quotes online at the click of a button.

- The flexibility of checking and comparing plans as per your convenience and time is unmatched. This means you can decide on which plan to buy from the comforts of your home and also buy including other family members in this decision.

Tools such as health insurance premium calculator available readily online helps you figure out your ability to pay and factor in some other aspects to know if a particular premium plan works for you or not.

In India, it is prudent to invest in Critical Illness (CI) and health insurance plans to avail of financial assistance against medical treatment costs for various health ailments and related hospitalization.

With the growing number of cancer patients in the country, however, it is advisable to consider buying a dedicated cancer insurance plan to help mitigate the financial burden related to cancer treatment expenses.

To help you understand, we are listing the key differences between health insurance, critical illness insurance and cancer insurance in the below table

| Type of Insurance | Cancer Insurance | Critical Illness Insurance | Health Insurance Plans |

|---|---|---|---|

|

Reason to Purchase |

|

|

|

|

What Does It Cover? |

|

|

|

|

Who Should Purchase? |

|

|

|

|

Rising Healthcare Costs |

|

|

|

Nowadays, having health insurance coverage has become a resourceful weapon against the rising costs of medical treatment. The Health insurance plans provide comprehensive financial assistance against the various in-patient hospitalisation and treatment expenses.

At the same time, you can enhance the health insurance coverage by augmenting your basic medical insurance policy with a Critical Illness (CI) and Cancer insurance plan. This way, you can avail of all-around financial protection against common and life-threatening ailments, including cancer. Be sure to check the health insurance claim settlement ratio before making the purchase.

Awareness about health insurance is a good thing, but it also provides impetus for misconceptions and notions to spread around like wildfire. Some common false notions include:

1. I am healthy, so I don’t need health insurance

Well, that’s certainly not true. Even when you’re health and young, investing in a health insurance benefits in the long run. You’re covered for any unpredictable health mishaps that might arise and you can also stay worry-free

2. I am a smoker so I can’t buy a health insurance plan

Insurance providers may charge a higher premium and extended waiting period as your smoking habit can give rise to complicated health conditions like lung cancer or respiratory problems and put you at a potential risk of developing a pre-existing disease before you buy the policy. But rest assured, smoking is not the basis for denying health insurance altogether.

3. If I couldn’t renew my health policy, all my benefits lapse

All insurance renewals offer a grace period up to 30 days post-due date wherein you can renew your policy without losing on any of your benefits and bonuses. So, this is a complete myth and not a reality.

Understanding your premium and coverage is only half the job. Knowing how to file a health insurance claim ensures you can actually use your policy when needed. Health insurance plans offer two types of claims, cashless and reimbursement, along with the convenient “Cashless Everywhere” feature for added flexibility.

1. Cashless Claim

This claim process allows you to receive treatment without paying the hospital bill upfront. The insurer settles the approved amount directly with the hospital.

Traditionally, cashless claims were available only at network hospitals. However, with the availability of ‘Cashless Everywhere’ feature, you can now avail of cashless treatment even at non-network hospitals, up to your sum-insured limit.

Here’s how the cashless claim process works:

-

Step 1: Inform the Insurer

For any planned treatment, inform at least 48 hours before admission.

For emergency treatment, inform the hospital within 48 hours of hospitalisation. -

Step 2. Get Pre-authorised Approval

Visit the hospital’s insurance desk with your ID proof and policy details.

Submit the pre-authorisation form along with the required documents.

Once approved by the insurer, you can proceed with cashless treatment. -

Step 3. Hospital Discharge

Sign off on the necessary medical and claim-related papers.

Pay yourself only for items such as hospital gowns, disposables, etc., that are not covered under your policy. -

Step 4. Claim Settlement

Your medical facility forwards the final bill to your insurer.

The insurer settles the sanctioned bill directly with your hospital.

2. Reimbursement Claim

This claim type is typically used when cashless treatment is unavailable, especially in cases involving non-network hospitals. Follow some simple steps to file a reimbursement plan.

-

Step 1. Inform Your Insurer

Notify the insurance company about your hospitalisation and continue the treatment. -

Step 2. Settle the Outstanding Hospital Bill

Clear the entire bill before leaving the hospital. Do preserve all original bills and other related medical documents for reimbursement. -

Step 3. Initiate the Claim

Fill out the claim form and submit it to the insurer within the specified time, along with the required documents. -

Step 4. Claim Settlement & Payment

The insurer reviews your submission and releases the approved claim amount directly to your bank account provided.

Knowing the difference between cashless vs reimbursement claims allows you to make the right choice during a health crisis and avoid unexpected medical costs.

Health Insurance FAQs

How Do I Choose A Health Insurance Plan?

What Are the Diseases Covered Under Health Insurance Policy?

Which Health Insurance Plan Covers Cancer?

Can We Claim Health Insurance Policy Immediately?

Can Cancer Patients Get Health Insurance Plan After Diagnosis?

How Soon Can I Use Health Insurance Policy?

Is It Worth Buying Critical Illness Insurance Policy?

Does Normal Health Insurance Plans Cover Critical Illness?

Is It Better to Take Critical Illness Policy or Health Insurance Plan?

In A Health Insurance Policy, What Does Cashless Hospitalisation Means?

How Can I Add My Family Members to My Existing Health Insurance Plan?

Can A Person Have More Than One Health Insurance Plans?

How Much Does Health Insurance Cost for An Individual?

Do Health Insurance Plans Cover Diagnostic Charges?

What Are the Documents Required for Buying A Health Insurance Plan?

Is Medical Test Mandatory to Purchase A Health Insurance Policy?

Is There Any Difference Between Health Insurance and A Mediclaim Policy?

How Do I Estimate the Cost of Health Insurance?

What is the right time to buy Health Insurance Plan?

How to Select the Best Health Insurance Plan in India?

How much Health Insurance cover do I need?

What happens to the policy after claim is filed?

Can someone buy health insurance policy if he/she is not an Indian National but living in India?

What are the maximum and minimum policy duration?

How does smoking affect health insurance premium?

What is the procedure for reimbursement settlement?

Why we should avail health insurance at an early age?

What is the best age to get health insurance?

What is a ‘Free Look Period’?

Can I buy more than one health insurance plan?

Is there any tax benefit with health insurance premiums?

What is waiting period in health insurance plans?

What if I already have a health insurance policy but just want to increase my sum insured?

Can I insure my husband?

Can Health Insurance be bought by a minor?

What is healthcare insurance?

Does a waiting period apply if I increase my sum insured at the time of renewal?

Which hospitals are part of the insurer’s network?

I’m young and healthy, do I still need health insurance?

Does health insurance cover maternity / pre-existing conditions / dental / outpatient?

How is “sum insured” decided and how much should I pick?

Is health insurance coverage valid pan-India/internationally?

Will my health insurance premium increase with age?

What factors should I compare while buying a health insurance policy?

Why does my premium increase?

Should I buy an individual plan or a family-floater/senior citizen plan/critical illness add-on?

ARN: PCP/HP/110823

Sources:

www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=89

www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=55

www.indiapost.gov.in/Financial/pages/content/post-office-saving-schemes.aspx

www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=134

www.incometaxindia.gov.in/Pages/tools/deduction-under-section-80c.aspx

www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11865&Mode=0

www.rbi.org.in/Scripts/FAQView.aspx?Id=79

www.forbes.com/advisor/in/health-insurance/how-to-choose-a-health-insurance-plan-for-your-family/

www.indiatoday.in/impact-feature/story/how-to-pick-the-best-health-insurance-policy-2325613-2023-01-24

www.hindustantimes.com/brand-post/a-step-by-step-guide-to-choosing-the-right-health-insurance-plan-101637838456000.html

www.thehindu.com/business/healthcare-cost-inflation-soaring-raising-health-cover-premiums/article69023505.ece

www.mohfw.gov.in/sites/default/files/NHA 2020-21_up.pdf

www.indiatoday.in/health/story/india-health-expenditure-rises-decline-direct-healthcare-cost-health-ministry-government-data-2606770-2024-09-26

www.downtoearth.org.in/health/indias-per-capita-health-expense-jumped-82-in-last-decade-national-health-accounts-estimates

www.financialexpress.com/business/healthcare/indias-healthcare-costs-to-rise-13-in-2025-beat-global-average-report/3800929/

www.businesstoday.in/union-budget/story/economic-survey-203-24-health-insurance-sector-to-grow-97-annually-over-the-next-5-years-438140-2024-07-22/

www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=89

www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=55

www.indiapost.gov.in/Financial/pages/content/post-office-saving-schemes.aspx

www.nsiindia.gov.in/InternalPage.aspx?Id_Pk=134

www.incometaxindia.gov.in/Pages/tools/deduction-under-section-80c.aspx

www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11865&Mode=0

www.rbi.org.in/Scripts/FAQView.aspx?Id=79

www.forbes.com/advisor/in/health-insurance/how-to-choose-a-health-insurance-plan-for-your-family/

www.indiatoday.in/impact-feature/story/how-to-pick-the-best-health-insurance-policy-2325613-2023-01-24

www.hindustantimes.com/brand-post/a-step-by-step-guide-to-choosing-the-right-health-insurance-plan-101637838456000.html

www.thehindu.com/business/healthcare-cost-inflation-soaring-raising-health-cover-premiums/article69023505.ece

www.mohfw.gov.in/sites/default/files/NHA 2020-21_up.pdf

www.indiatoday.in/health/story/india-health-expenditure-rises-decline-direct-healthcare-cost-health-ministry-government-data-2606770-2024-09-26

www.downtoearth.org.in/health/indias-per-capita-health-expense-jumped-82-in-last-decade-national-health-accounts-estimates

www.financialexpress.com/business/healthcare/indias-healthcare-costs-to-rise-13-in-2025-beat-global-average-report/3800929/

www.businesstoday.in/union-budget/story/economic-survey-203-24-health-insurance-sector-to-grow-97-annually-over-the-next-5-years-438140-2024-07-22/

More plans for you

-

2 Crore

2 Crore

Term PlanAffordable financial security of your loved ones

Terminal illness cover at zero additional cost

Tax deduction u/s 80C of Income Tax Act, 1961

Multiple payout options - Monthly income and lump sum

-

NRI

NRI

Life InsuranceHassle-free worldwide$+ claim processing

Flexible premium payment options

GST waiver~4 of up to 18% for eligible customers

Video medical test at your own ease

-

Guaranteed

Guaranteed

Income PlanGuaranteed maturity benefit to help achieve future goals

Multiple plan variants to choose from

Tax deduction u/s 80C of Income Tax Act, 1961

Death benefit on policyholder's demise's during policy term

-

Axis Max Life Smart Fixed-return Digital Plan

Axis Max Life Smart Fixed-return Digital PlanBuilt-in life cover

Tax deduction u/s 80C of Income Tax Act, 1961

Tax-free## fixed returns up to 6.80%** u/s 10(10D)

Facility to avail a loan in case of a financial emergency

We would like to hear from you

Let us know about your experience or any feedback that might help us serve you better in future.

Related Articles

What Is Health Insurance?

Health insurance is a type of insurance that covers medical expenses incurred on an illnessor injury. These medical expenses include…

Read More

Benefits of Health Insurance

Health issues have become an increasingly pressing concern in the past few years. The average persons lifestyle today involves greater…

Read More

What is Mediclaim?

if this is one of the questions that is keeping you from getting comprehensive financial security for your health, then we are here to help…

Read More

Online Sales Helpline

- Whatsapp: +91-7428396005Send ‘Quick Help’ from your registered mobile number

- Phone: +91-124-648-890009:30 AM to 06:30 PM (Monday to Sunday except National Holidays)

- service.helpdesk@axismaxlife.comPlease write to us incase of any escalation/feedback/queries.

Customer Service

- Whatsapp: +91-7428396005Send ‘Hi’ from your registered mobile number

- 1860-120-55779:00 AM to 6:00 PM (Monday to Saturday)

- service.helpdesk@axismaxlife.comPlease write to us incase of any escalation/feedback/queries.

NRI Helpdesk

- +91-11-71025900 , +91-11-61329950 (Available 24X7 Monday to Sunday)

- nri.helpdesk@axismaxlife.comPlease write to us incase of any escalation/feedback/queries.

Popular Searches

PageLast updated on 9th July 2026WebsiteLast updated on 24th December 2025

![<span class="text-[18px] text-darkBlue dark-theme-font font-bold">

15% Discount

</span>

<br>

<span class="text-[18px] font-semibold font-family-lato">

For Salaried<sup>3</sup>

</span>](https://www.axismaxlife.com/static-page/assets/homepage/term-sticky-desktop-piggy.svg)