Individual

Individual

You did it!

Here's how you performed

You're making informed choices!

Being well informed puts you in a stronger position to plan for life's uncertainties.

Take the Quiz!

Take the Quiz!A ULIP plan is perfect for:

These plans are a good fit if you are saving money for your retirement or child’s education, etc.

Depending on your risk appetite, you may choose funds such as equities, debt, or other asset classes.

Whether you are nurturing a family or planning to retire, ULIPs can help you achieve goals at any stage in your lifetime.

One benefit of starting early is that the premiums are affordable, and your investment will have more time to grow.

Ideal if you want dual benefits of investment and insurance in a single plan.

Working professionals can create a retirement fund by availing long-term capital appreciation while adjusting their investment based on market conditions.

A Unit-Linked Insurance Plan (ULIP) is a financial product that combines the benefits of life insurance cover and investment in one plan. When a policyholder buys a ULIP, a portion of the premium paid goes towards securing the life insurance plan and the remainder is invested.

ULIPs offer a high degree of flexibility, allowing you to invest across funds based on your risk appetite. Because returns are market-linked, ULIPs are best suited to long-term goals — wealth creation or retirement.

Under a ULIP, the investment risk in the portfolio is borne by you as the policyholder. Here is what happens to every premium you pay:

A portion goes to your life insurance cover; the rest is invested in the equity and debt fund options you choose.

The invested corpus is divided into ‘units’ with a specific face value, allocated in proportion to your investment.

Each unit's value is its Net Asset Value (NAV), reflecting increases or decreases in the underlying assets.

Partial withdrawals after the lock-in sell the corresponding number of units at prevailing NAV.

Maximal wealth appreciation through market-linked instruments while your life cover protects your family.

Move between equity and debt funds at any time during the policy term, with a fixed number of free switches each year.

Redirect future premiums between available fund options at any time to match your evolving goals.

After the 5-year lock-in, make a fixed number of partial withdrawals from your fund value without additional charges.

Receive the fund value at maturity, built through disciplined long-term market-linked investing.

Your nominee receives the higher of sum assured or fund value, keeping your family's goals secure.

Stay invested longer and earn extra units added to your fund value as a reward for continued premiums.

Align fund choices with life goals — education, home, retirement — on one flexible platform.

Buying a ULIP is a viable strategy to grow your savings through market-linked returns while staying protected. The global ULIP market was valued at $1.1 trillion (Allied Market Research, Aug'25) — and for good reason:

Manage your money — change fund allotments to secure or grow your corpus as markets move.

Track NAVs and fund performance openly; you always know where your money is invested.

Comprehensive maturity and death benefits keep your family's future protected.

Healthy market-linked returns in the long run, plus significant tax savings as per prevailing laws.

A ULIP plan is perfect for:

A good fit if you are saving for retirement, a child's education, or another distant milestone.

Choose equities, debt, or balanced funds depending on how much risk you're comfortable taking.

Whether you're nurturing a family or planning to retire, ULIPs adapt to your stage of life.

Start early: premiums are affordable and your investment gets the longest runway to compound.

Ideal if you want long-term financial goals and life cover handled in a single product.

Keep these four things in mind while choosing the best unit linked insurance plan in India:

Equities offer high growth potential for the long term; debt funds offer stability. Match the mix to each goal.

Size your cover to long-term goals such as your children's higher education or your retirement.

Staying invested 10–15 years helps grow wealth and beat volatility (Kotak Institutional Equities, 2024).

Compare plans on 80C deductions and 10(10D) maturity benefits under prevailing tax laws.

ULIPs channel your premiums into professionally managed, market-linked funds while compounding works over the policy term. Loyalty additions, fund switches, and top-ups let you steer the corpus toward your goals as markets and life circumstances change.

Map each financial goal to a time horizon before allocating funds: shorter horizons favour debt-oriented funds; longer horizons can carry more equity exposure. Review the mapping annually so your allocation always matches the years remaining to each goal.

Strengthen your base cover with optional riders available on Axis Max Life plans:

Pays a lump sum on diagnosis of listed critical illnesses or disability, cushioning income shocks during treatment.

Enhances protection with additional cover options for accidental death and disability at a nominal extra premium.

Buying a ULIP from Axis Max Life Insurance takes just a few minutes:

Go to the official Axis Max Life Insurance website.

Select Investment Plan and enter your name, date of birth, gender, etc.

Click ‘View Plans’ and explore the products listed.

Enter personal details, check your premium estimate and click ‘Proceed’.

Select Net Banking, Credit Card, UPI, or another payment option.

Complete the payment and enjoy the perks of your ULIP.

Like other life insurance plans, you must meet a few prerequisites before buying a ULIP:

You must fall within the plan's minimum and maximum entry age; limits vary by product.

Resident status requirements apply; NRIs may be eligible subject to plan terms.

Keep identity, address, and income proofs handy for a smooth KYC process.

A medical examination may be required depending on age and the cover you choose.

How ULIPs compare against other popular instruments on the parameters that matter:

| Option | Life Cover | Market-Linked Returns | Tax Benefit* | Lock-in |

|---|---|---|---|---|

| ULIP | ✓ Included | ✓ Equity & debt funds | 80C + 10(10D) | 5 years |

| Mutual Funds | ✗ None | ✓ Market-linked | ELSS only | None / 3 yrs (ELSS) |

| Traditional Life Insurance | ✓ Included | ✗ Fixed/bonus based | 80C | Policy term |

| PPF | ✗ None | ✗ Fixed, govt-set | 80C (EEE) | 15 years |

| NPS | ✗ None | ✓ Market-linked | 80C + 80CCD(1B) | Till age 60 |

| Fixed Deposits | ✗ None | ✗ Fixed rate | Tax-saver FD only | Varies / 5 yrs |

See how much wealth your ULIP can build. Get your personalised premium estimate in under 2 minutes.

Check PremiumFreedom to choose your retirement age · Partner Care Rider for spouse security · equity-linked returns with downside protection · guaranteed loyalty additions from the 10th policy year · "Save more tomorrow" top-ups · tax benefits on premiums.

Flexible premium and policy terms with wealth boosters, wide fund choice, and life cover — built to flex with your goals.

Inbuilt life cover with zero policy-admin and premium-allocation charges — more of your premium gets invested.

Secure your child's education with equity participation, multiple fund options, and premium funding on death.

| ULIP Plan Name | Key Features & Benefits |

|---|---|

| Axis Max Life Fast Track Super Plan | Achieve long-term goals while securing your future; multiple fund strategies. |

| Axis Max Life Platinum Wealth Plan | Secure your family's future with comprehensive maturity and death benefits. |

| Axis Max Life Online Savings Plan — Variant 1 | Inbuilt life cover with flexibility to increase cover; zero allocation charges. |

| Axis Max Life Online Savings Plan — Variant 2 | Triple protection: lump sum payout, monthly income, and premium waiver. |

| Axis Max Life Shiksha Plus Super Plan | Equity-market participation with multiple fund options for a child's future. |

Build a retirement corpus during your earning years; annuity-ready payouts when you stop working.

Equity-oriented plans focused on maximising long-term wealth appreciation.

Goal-protected plans that fund your child's milestones even in your absence.

Snapshot of flagship funds against their benchmarks (5-year returns):

Open-ended multi-cap equity fund focusing on midcaps with long-term high-growth potential.

Open-ended debt fund with preference for government securities, suited to systematic transfer plans.

See the full fund list with 1/3/5-year returns in the fund cards carousel on the Investment Plans page. Past performance is not indicative of future returns.

Invests in government securities and corporate bonds — stability first, steady returns.

Invests in stocks for high growth potential over long horizons; higher volatility.

Blends equity and debt to balance growth with downside cushioning.

The longer your money stays invested, the more compounding works in your favour.

Stay invested beyond the lock-in; ULIPs reward long-term discipline with loyalty additions.

Diversify across equity and debt funds in line with your risk appetite.

Use free fund switches to rebalance as markets and life goals change.

Claim deductions u/s 80C and tax-free maturity u/s 10(10D), as per prevailing tax laws.

An effective ULIP strategy aligns fund selection with goals and horizon: begin equity-heavy while goals are distant, glide toward debt as they approach, use top-ups in market dips, and let loyalty additions accumulate by staying the full term.

A ULIP calculator is a tool that helps you determine the maturity amount under a unit linked insurance plan based on your monthly investment, tenure, and expected growth rate.

You get: ₹20k/month invested in 2005 would have been

₹4.31 Cr nowCompounding grows your investments with time. An illustration for a Wealth Plan at ₹10,000/month over a 10-year investment tenure, held for 20 years:

| Type of ULIP | Monthly Contribution | Investment Tenure | Corpus after 20 yrs @4% p.a. | Corpus after 20 yrs @8% p.a. |

|---|---|---|---|---|

| Wealth Plan | ₹10,000 | 10 years | Illustrative corpus at 4% | Illustrative corpus at 8% |

Assumed rates of 4% and 8% p.a. are illustrative only, as per IRDAI-permitted illustrations; actual returns depend on fund performance.

Premiums paid qualify for deduction under Section 80C (old tax regime).

Maturity benefits are exempt u/s 10(10D), subject to prescribed premium conditions.

If annual ULIP premiums exceed ₹2.5 lakh, returns on the excess become taxable as per current rules.

Claim the exemption (up to ₹1.5 lakh under 80C) when filing your return by declaring the ULIP premium under eligible deductions, retaining premium receipts and the policy statement as proof. Maturity proceeds are reported under exempt income u/s 10(10D) where conditions are met.

Know the charges before you invest — many Axis Max Life online plans waive several of these:

Deducted upfront from premium before units are allocated.

Annual charge for managing the fund, adjusted in NAV.

Monthly charge for policy servicing and administration.

Cost of the life cover, based on age and sum at risk.

Applies if the policy is discontinued during the lock-in.

May apply after you exhaust your free fund switches.

May apply on redirecting future premiums beyond free limits.

May apply beyond the free partial-withdrawal limit post lock-in.

Not comfortable managing investments? Opt for systematic, rule-based switching managed for you.

Change premium allocation yourself based on your investment view and goals.

Invest surplus money over and above premiums to accelerate wealth appreciation.

Monitoring NAV shows your fund's performance relative to benchmarks.

Use economic indicators and market trends to rebalance via free switches.

Know what you're investing for from the very beginning.

Choose equity, debt, or balanced funds based on the risk you can carry.

Understand every charge so you know exactly what reaches the market.

Past results don't guarantee success, but they reflect fund quality.

Pick ULIPs that flex with life changes, and plan around the 5-year lock-in.

ULIPs are designed for long-term wealth creation, not quick profits.

Check your fund's progress regularly and switch when consistently underperforming.

Mortality, admin, and fund-management charges affect net returns — know them.

Early withdrawals break the force of compounding and limit potential gains.

Always invest with a clear goal so fund choices and tenure fit the purpose.

ULIPs suit disciplined, goal-based investors with a medium-to-long horizon who want market participation without giving up life cover — from young professionals starting early to families planning education and retirement milestones.

Popularity brings misconceptions. Here's the myth vs. the fact:

The ULIP lock-in period is a mandatory feature that promotes disciplined, goal-oriented investing. After 5 years, partial withdrawals unlock — and staying invested longer keeps compounding and loyalty additions working.

ULIPs suit those seeking long-term options: market conditions may affect short-term returns, but a long investment term supports compounding through cycles. For retirement, children's education or marriage, and wealth building, risk-adjusted fund choices keep the plan aligned to your comfort.

Total current value of the units you hold across funds.

The guaranteed life-cover amount paid to your nominee.

Moving your money between equity, debt, and balanced funds.

Amount payable if you exit the policy before maturity.

Fees like allocation, fund management, and mortality charges.

Per-unit value of the fund, updated with market movement.

A ULIP bought with one lump-sum premium payment.

Optional add-on covers like critical illness or accident protection.

Raising a claim against the life coverage under your ULIP is simple:

Notify Axis Max Life online, by phone, or at a branch to initiate the claim.

Provide the policy document, claimant's ID, and other required proofs.

The claim is assessed and, once approved, settled to the nominee's account.

Even though Shyam invested ₹18 lakh MORE than Ram, his retirement corpus is significantly smaller!

Due to Ram's longer investment period, the power of compounding worked in his favor. He ended up with a retirement corpus that is almost ₹1 crore larger than Shyam's, despite investing significantly less!

It is recommended to invest in a mix of different asset classes like government schemes (like PPF) and market-linked investment products (like mutual funds) to get good returns. However, keep in mind your financial goals, risk appetite, and investment tenure before you begin. For long-term goals, consider investing in ULIPs, 5-year fixed deposits (FDs).

For short-term goals, 1 to 3-year FDs, liquid funds, corporate FDs, etc are good. In contrast, if you are planning your retirement goals, you have options like NPS, pension plans, voluntary provident fund (VPF), etc.

To earn higher returns, you need to invest in instruments with higher risk levels, such as market-linked plans, stocks, and equities. These investment instruments generally require investment for a long term. Here is a list of high-risk investment options that offer higher returns over the long term:

Irrespective of the amount you wish to invest, it is prudent to assess your risk appetite along with your investment tenure. If you do not want to take a risk, consider investment options like a post office FD or a bank fixed deposit. You can earn an attractive rate of return based on the investment tenure you select.

You can also invest in liquid mutual funds of your choice if you are willing to take additional risk.

To earn a monthly income from your investment of 20 lakhs, you can consider investment in a mix of safe and market-linked instruments. Before you begin, assess your risk appetite, financial goals, and amount per instrument.

Some low-risk, secured investment instruments are fixed deposits, post office monthly income scheme, and senior citizen savings scheme, etc. High-risk, high-returns investment options include unit-linked insurance plans, stocks, and real estate investments, etc.

The choice of investment would depend on multiple factors, including your age, risk appetite, and expected income from the investment. Some options include

However, it is advisable not to invest your corpus in any one instrument.

Here are the common mistakes which you need to be mindful of. Make sure to avoid them:

If missed/delayed payments start piling up, then it will severely lower your credit score. So, pay your EMIs or credit card bills on time.

Moreover, lenders might feel that you’ll use up the credit of all the cards even if you don’t use all of the available credit. It’s one of the common mistakes that impact credit scores. So, it’s best to avoid it.

Otherwise, it will hurt your overall credit report and decrease your credit score.

When someone has multiple unsecured loans, it indicates he/she might be financially overburdened with debt. Furthermore, it denotes such persons as risky candidates. Lastly, always remember that if you have numerous active unsecured loans, it’ll have a major negative impact on your credit score.

Apart from lowering your credit score, there’s another side effect. It cuts down on your negotiating options with the lender. As a result, you might receive credit, but on unfavourable terms and conditions.

Late payments might remain recorded in the credit report for many years. You will face questions regarding late bill payments if you apply for loans. You can set payment reminders or set up the auto-pay option to avoid late payments.

You should try your best not to let the credit utilisation rate rise above 30%. Otherwise, your credit score can come down greatly. So, what can you consider? Try to pay off your credit card dues in time. Use other payment methods until you’ve cleared your credit card dues.

Moreover, if you track your credit report regularly, then you’ll also come to know when your credit score is on the fall and take steps to rectify the situation.

Building a good credit record can be time-consuming. So, develop good financial habits early on and consciously avoid making the 10 common mistakes that can decrease your credit score. It will be easy for you to build creditworthiness.

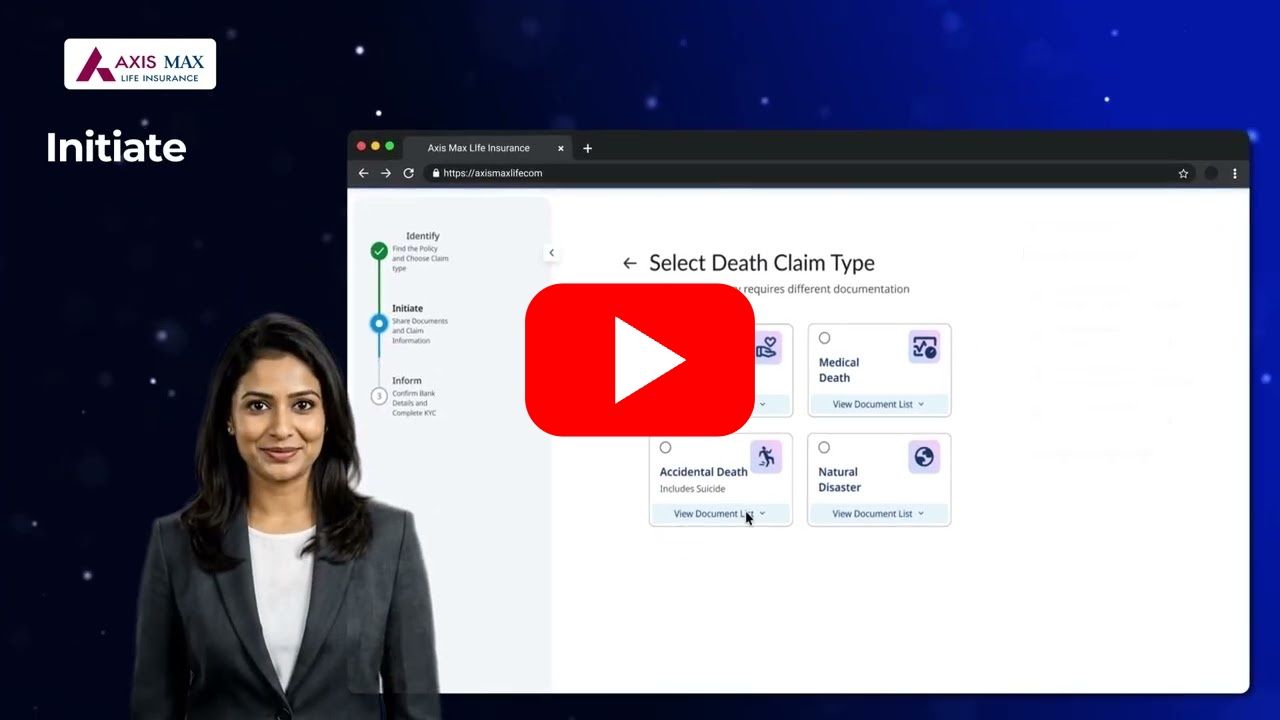

Watch How to File a Claim Online

A term insurance plan provides a large life cover at an affordable premium. If the policyholder passes away during the policy term, the nominee receives the full sum assured as a death benefit.

The sum assured in a term plan is typically recommended to be 10–15 times your annual income to ensure your family can maintain their standard of living and meet long-term financial obligations.

Term insurance premiums are determined by the policyholder's age, health, lifestyle habits, sum assured, and policy term. Buying at a younger age locks in lower premiums for the entire duration.

Was the Information Helpful?

Very Good

Learn the basics of how credit score is calculated, what are the factors impacting your credit score and the key benefits of having a good credit score in India.

Read More

A good credit score is important when applying for a new loan or credit card. Know 5 ways to easily increase your credit score to improve your eligibility for additional credit.

Read More

Power of Compounding can help you secure the long-term goals while planning your investments better. Use Power of Compounding Calculator to check the math on Max Life Insurance.

Read MoreReal questions and top answers from Reddit communities - unfiltered opinions from actual policyholders and financial planners.

These are independent user opinions from Reddit and do not represent the views of Axis Max Life Insurance. Clicking a card opens the original discussion on Reddit.

Watch How to File a Claim Online

Watch How to File a Claim Online

Watch How to File a Claim Online

Watch How to File a Claim Online

How Much Pension Do You Want Every Month?

Watch How to File a Claim Online

Axis Max Life Smart Secure Term Insurance Plans

1 Crore

Documents you'll need

You will need a few documents to get started. If something is missing right now, it's ok. We'll guide you as you go.

Indian

Indian

Watch How to File a Claim Online

Under a unit linked insurance plan (ULIP), the investment risk in the portfolio is borne by you (as a policyholder.) The primary purpose of buying the best ULIP is to secure your loved ones financially against any unforeseen events.